What’s the ROI of Hiring a Fractional CFO for a $5M–$20M Business?

As your team considers bringing on a fractional CFO, the natural question arises: what’s the real ROI on this temporary hire? How does it compare in value to a full-time CFO? The honest answer is that the return is real and usually several times the cost, but you have to know where to look for it. Here is where the value actually comes from, with the kind of numbers that make it concrete, because vague claims about value are worth nothing to a founder weighing a real decision.

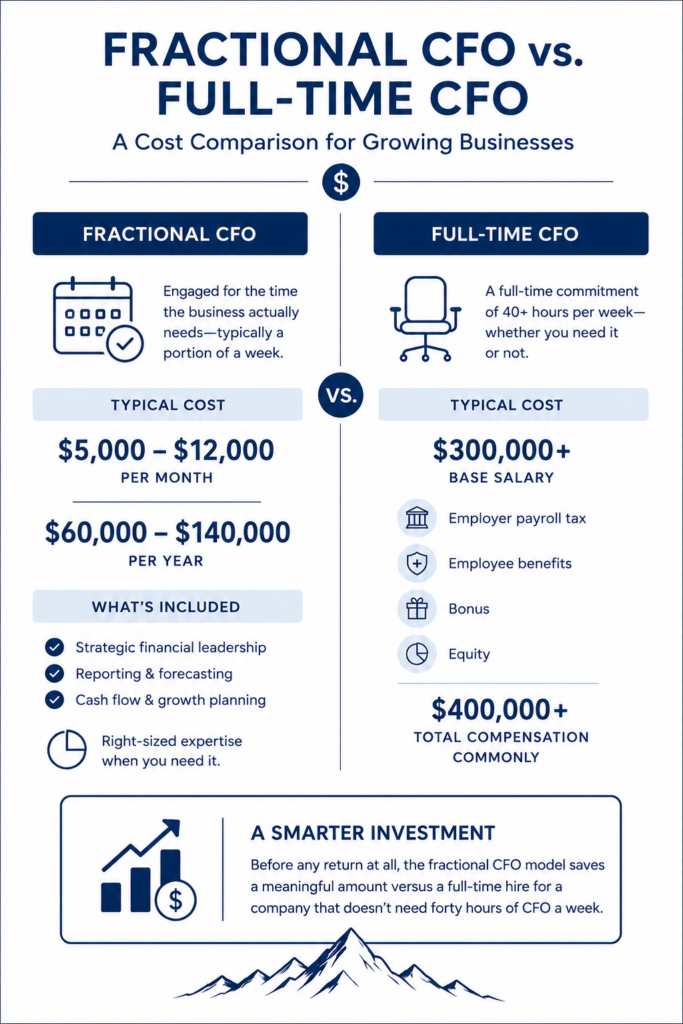

Start With What It Actually Costs

Set the baseline first. A full-time CFO at a growing company runs $300,000 and up in total compensation, frequently with equity and bonus on top, plus the cost and risk of recruiting for a senior role you may not be able to keep busy full-time at $8M in revenue.

A fractional CFO is engaged for the time the business actually needs, which for a $5M–$20M company is typically a portion of a week. The cost commonly lands somewhere in the range of $5,000 to $12,000 a month depending on scope and intensity, call it $60,000 to $140,000 a year. Compare this against a full-time equivalent of $300,000-plus salary – before employer payroll tax, employee benefits, bonus, and equity. So before any return at all, the model saves a meaningful amount versus a full-time hire for a company that does not need forty hours of CFO a week.

That is the cost side. Now the return, in the categories where it actually shows up.

Where the Return Comes From

1. Cash freed from working capital

This is the most concrete and often the fastest payback. A fractional CFO who tightens the cash conversion cycle, collecting in 40 days instead of 60, right-sizing inventory, renegotiating vendor terms, frees cash that was trapped inside the operation. For a $10M business carrying a 60-day cycle, shaving 15 days off can free several hundred thousand dollars of cash, money you would otherwise have borrowed or raised. That is not a soft benefit. It is cash back in the account, and it frequently covers the annual cost of the engagement several times over in the first year alone.

2. Capital raised, and raised on better terms

When a company takes on debt or raises equity, the quality of its financials and forecasts directly affects the outcome. A fractional CFO who walks into a lender conversation with investor-grade financials and a defensible model gets a larger facility at a lower rate than a founder presenting cash-basis books and a forecast in their head. On a $2M credit facility, a single point of rate difference is $20,000 a year. On an equity raise, the difference between a clean process and a messy one can be a materially better valuation or the difference between closing and not closing. The CFO’s fee is small against the size of the capital decisions they shape.

3. Margin and profitability improvement

A fractional CFO who breaks blended numbers down by customer, product, and line shows you which parts of the business actually make money. Acting on that, pricing up the underpriced work, cutting or fixing the lines that lose money, focusing growth on the profitable segments, moves the margin. On a $10M business, a two-point gross margin improvement is $200,000 a year, recurring. Margin gains compound, and they survive long after the engagement, which makes this one of the highest-return categories over time.

4. The expensive decisions you don’t make

This one is invisible by nature, which is exactly why it is undervalued. The location that looked profitable but would have drained cash for two years. The hire made too early against a sales ramp that was never going to close in time. The contract signed without anyone modeling what it did to working capital. A fractional CFO who models the big decisions before you commit prevents the costly wrong ones. A single avoided mistake at this scale, a bad expansion, a six-figure cash surprise, can exceed a full year of the CFO’s cost. You never see this return on a statement because the loss never happened, but it is among the largest.

5. Faster, better decisions

Beyond avoiding the wrong moves, a fractional CFO lets you make the right ones with confidence and speed. The founder who can see, in a model, what a decision does to cash and the business over the next eighteen months commits faster and more often than the one waiting until they feel sure. In a growing market, the cost of a decision delayed three months because nobody could analyze it is real, even if it never gets measured. Decision speed backed by analysis is a return that does not fit neatly on a spreadsheet but shows up in how fast the company can move.

6. A higher number when you sell

For a founder thinking about an eventual exit, this is the largest category of all. A company sells on a multiple of EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), and a fractional CFO who improves margins, cleans the financials, builds a defensible adjusted-EBITDA story, and reduces the business’s dependence on the founder raises both the multiple and the base number. On a business selling for eight times EBITDA, every $100,000 of durable EBITDA the CFO helps build is worth $800,000 in enterprise value. Years of fractional CFO fees can be returned many times over in a single transaction.

7. Your time and focus back

The founder who is doing the financial thinking themselves, at night, between everything else, is paying a cost that does not appear anywhere. A fractional CFO takes the financial weight off the founder’s plate and gives the largest decisions a real owner, freeing the founder to run the business they are actually best at running. Hard to put a number on, easy to feel, and consistently one of the first things founders mention after the fact.

Doing the Math for Your Own Business

Add it up and the pattern is consistent. A $5M–$20M company paying $60,000 to $140,000 a year for fractional CFO leadership is typically looking at returns, in freed cash, better capital terms, margin gains, and avoided mistakes, that run several times the cost in the first year, before counting the exit-value lift that may dwarf everything else later. The reason the ROI feels unproven before you start is that the costs are visible and the returns are diffuse. Once you know the categories, the math usually answers itself.

The honest caveat: the return depends on the CFO actually doing this work and on the business having room to improve. A company with already-pristine cash management, perfect margins, and no upcoming capital decisions has less to gain. Most $5M–$20M companies are not that company. Most have working capital sitting idle, blended numbers hiding unprofitable segments, a capital decision on the horizon, and big choices being made without anyone modeling them. That is where the return lives.

Speak to a CFO

The fastest way to answer the ROI question for your specific business is to have someone look at it and tell you where the return would actually come from, the freed cash, the margin, the capital terms, the decisions ahead. That conversation is concrete, not theoretical, and it usually surfaces the answer quickly.

Get right-sized financial leadership from experienced CFOs ready to lead your team.

Book a CFO strategy call with Ascent CFO Solutions and get a straight read on what fractional CFO leadership would actually return for your business.

FAQs About Fractional CFO ROI

1. How fast does a fractional CFO pay for itself?

For most $5M–$20M companies with room to improve, the first measurable return, usually cash freed from working capital, arrives within the first few months and often covers the annual cost on its own. The larger returns, margin improvement, better capital terms, avoided mistakes, accrue over the engagement. Exit-value lift, if a sale is on the horizon, lands later and is typically the largest of all.

2. What does a fractional CFO actually cost?

Commonly $5,000 to $12,000 a month for a $5M–$20M company, depending on scope and how intensive the engagement is, which works out to roughly $60,000 to $140,000 a year. Compare that to $250,000-plus in total compensation for a full-time CFO, for a company that usually does not need a CFO forty hours a week.

3. Isn’t this only worth it if we are about to raise or sell?

A raise or a sale makes the return especially large, but it is not the only source. Freed working capital, margin improvement, better lending terms, and avoided mistakes accrue to companies that have no transaction on the horizon at all. The everyday return, cleaner cash, sharper decisions, better margins, stands on its own. A transaction just adds a large bonus category on top.

4. How do I measure the ROI if some of it is invisible?

Track what you can: cash freed from the working-capital cycle, rate and size improvements on financing, margin movement by segment. Acknowledge the categories you cannot fully measure, avoided mistakes and decision speed, while recognizing they are real. The visible categories alone usually justify the cost; the invisible ones are upside. The key is not to dismiss a return simply because it does not arrive with a label.

5. What if we already have a controller and a bookkeeper?

Then you have the backward-looking function covered, accuracy, the close, compliance, and you are missing the forward-looking layer, which is where the ROI in this article comes from. A fractional CFO sits above the accounting function you already have. It is not a replacement for your controller; it is the strategic layer your controller’s role does not include.

The Return Is Real, You Just Have to Know Where It Lives

The founders who hesitate on a fractional CFO are usually doing honest math with incomplete categories. They see the monthly cost and weigh it against a vague sense of “strategic value,” and the case looks shaky. The founders who say yes have learned to see the return where it actually shows up: in cash freed, margins moved, capital terms improved, mistakes not made, and an eventual exit worth more. By those categories, for most companies between $5M and $20M, the math is not close.

We help founders and CEOs of growth-stage companies across the country capture exactly these returns, freeing trapped cash, improving margins, securing better capital, and making the big decisions with someone modeling them first. Through our fractional CFO services, we deliver CFO-level leadership scaled to what your business actually needs, at a fraction of the full-time cost.

Book a CFO strategy call with Ascent CFO Solutions and find out what the real return would be for your business.