Fractional CFOs for SaaS Companies: What to Look for in a Part-Time Finance Leader

You are in a board meeting and an investor asks how your net revenue retention has moved over the last three quarters and what it implies about your CAC payback. You have a number somewhere, but you are not certain it is calculated the way they mean it, and you cannot speak to the trend with confidence. The meeting moves on. The moment stays with you, because it was the moment you realized the company has outgrown running finance off a bookkeeper and your own instincts, and you do not have anyone who owns these answers.

That is the situation a fractional CFO exists for at a SaaS company. You are past the point where a bookkeeper and a founder’s gut are enough, but a full-time CFO at $250,000 and up does not fit a business doing a few million in ARR. You need CFO-level financial leadership on the metrics, the model, and the board, without a full-time hire. The question is who, and SaaS raises the bar on that answer in ways most industries do not.

SaaS finance carries complexity that does not show up in services, manufacturing, or even traditional product companies. Subscription revenue, deferred revenue accounting, the SaaS-specific metrics investors actually grade you on, and a board cadence that moves faster than other industries all combine to make the fractional role harder to fill well. A part-time generalist will know the names of the things that matter and miss the substance. The right fractional CFO knows SaaS cold and brings it on the days you actually need it. This article walks through what to look for.

Why SaaS Fractional CFO Roles Are Different

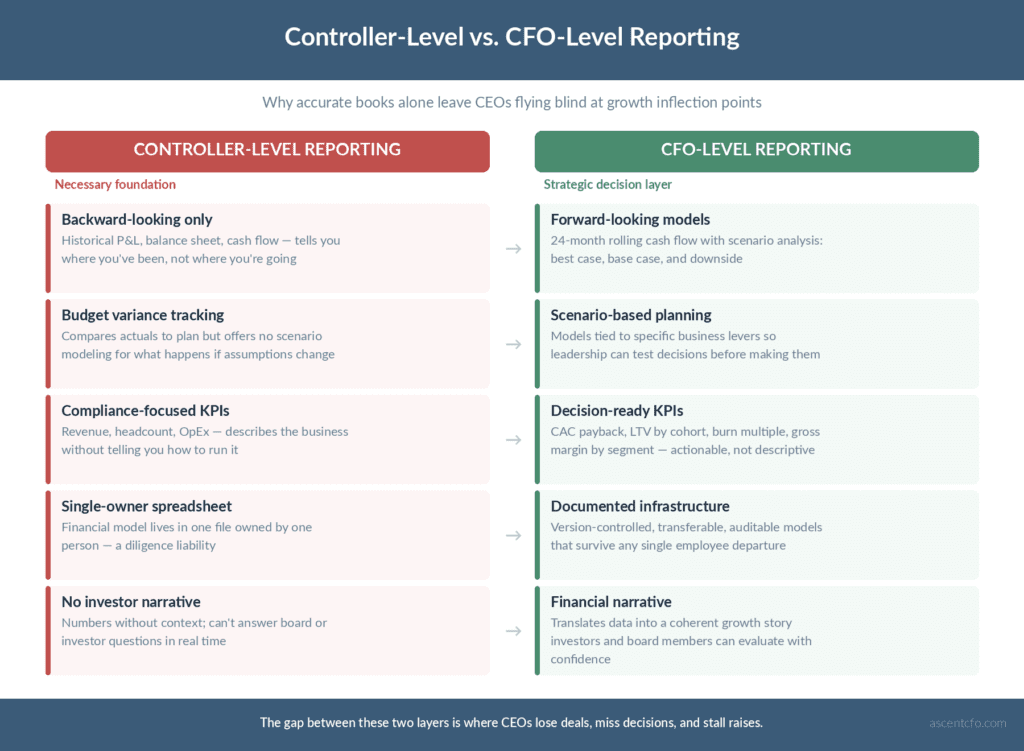

Most fractional CFO arrangements were built around businesses where clean books, a budget, and a cash forecast are the main deliverables. Those matter at a SaaS company too, but they are not the whole job, and a part-time finance leader who only does that work will leave the SaaS-specific gaps wide open.

A SaaS company’s financial discipline is judged on a different standard. Investors, boards, and acquirers grade the business on metrics unique to subscription models: net revenue retention, gross retention, customer acquisition cost, lifetime value, payback period, ARR growth rate, magic number, and the rule of 40. Those metrics need to be calculated correctly, tracked over time, defensible under questioning, and consistent with how revenue is actually recognized. A finance leader who has not lived inside a SaaS P&L will know the names. The one who can explain how NRR (Net Revenue Retention, the percentage of recurring revenue retained after expansion and contraction) behaves when a customer expands, contracts, and churns inside the same quarter is the one who has done this work before.

Revenue recognition is the second piece. ASC 606 (the accounting standard governing how subscription revenue is recognized over time) is not optional and not simple. A SaaS company with even modest contract complexity has multi-element arrangements, performance obligations, contract modifications, and deferred revenue running through the books every month. A fractional CFO who is not fluent in ASC 606 will let financials build up that do not survive an audit, a diligence process, or a sharp board member’s questions, and you will not find out until the worst possible moment.

The third piece is pace. SaaS companies move on a faster financial cadence than most industries: monthly board reporting, mid-month forecast updates, investor pings about a single metric. A fractional CFO has limited hours by design, which makes the ability to read your operating reality quickly and stay current between sessions essential. Someone who needs to re-learn the business every time they log in is the wrong fit for a part-time SaaS engagement.

The Six Things to Look for in a SaaS Fractional CFO

Six attributes separate the SaaS fractional CFOs who add real value from the ones who function as an expensive part-time bookkeeper. The list is in the order you should check them.

1. SaaS Metrics Fluency

The candidate should be able to explain, without notes, the difference between MRR (Monthly Recurring Revenue) and committed MRR, between gross retention and net revenue retention, between booked ARR and live ARR, and between contracted ACV (Annual Contract Value) and recognized revenue.

Beyond the definitions, they should be able to explain how each metric behaves under contract modifications, mid-period changes, and partial cancellations. The candidate who has opinions about how your specific business should report these metrics, given how your contracts are actually structured, is the one who has done this before.

The check: ask them to walk you through how your company’s metrics should be calculated based on your real contract patterns. A real SaaS CFO will have substantive opinions inside ten minutes.

2. Revenue Recognition Expertise

ASC 606 fluency is the price of admission for a SaaS fractional CFO. The candidate should be able to explain how your specific contract structures map to performance obligations, how multi-year deals get recognized, how mid-term modifications get accounted for, and how the deferred revenue waterfall moves period over period.

The risk of getting this wrong is concrete, and a part-time arrangement does not reduce it. Rev rec mistakes that pile up over a few months become a problem during the next audit, the next diligence process, or the next transaction, and cleaning them up after the fact is one of the more painful and expensive things a SaaS finance team can be asked to do.

The check: ask the candidate how they would handle a specific contract scenario from your business, like a multi-year prepay, a usage-based component, or a mid-term upgrade. The depth of the answer tells you everything.

3. Board and Investor Communication Track Record

A SaaS fractional CFO will be in front of, or directly preparing you for, your board within their first month. They need to be comfortable with the format: the metrics deck, the operating review, the runway scenario, the deferred revenue rollforward, the cohort analysis, the questions sophisticated investors ask, and the answers those investors expect.

Someone who has run or supported the CFO seat at a venture-backed or PE-backed SaaS company has done this. Someone who has only kept the books at a private services firm has not. The skills do not transfer cleanly enough to learn on the job during a board cycle, and a fractional CFO who cannot strengthen your board communication is missing one of the highest-value things the role provides.

The check: ask them to walk you through the last SaaS board meeting they prepared for or presented at. What was on the agenda, what the hardest question was, how it got answered.

4. Forecasting Discipline at SaaS Pace

SaaS companies forecast more frequently and at higher resolution than most businesses. Bookings forecasts updated regularly, cash forecasts kept current, the operating model rerun against new actuals, hiring plans tied to ARR milestones. The forecast is the operating spine of the business, not a quarterly artifact.

A strong SaaS fractional CFO can pick up your existing model and run scenarios on it quickly, or rebuild a workable model from your operating data in two to three weeks if the existing one is unusable. What you do not want is a part-time leader who treats the model as a once-a-year exercise, because at SaaS pace a stale model is a model nobody trusts when a real decision lands.

The check: ask the candidate to walk you through an operating model they built or ran at a SaaS company. What the assumption layer looked like, how scenarios were structured, how often it got updated.

5. Fluency in the SaaS Finance Stack

The modern SaaS finance function runs on a specific set of tools: NetSuite or Sage Intacct as the ERP, a subscription billing platform like Maxio (formerly SaaSOptics), Stripe Billing, or Chargebee, a revenue recognition tool that may or may not be the billing platform, equity management on Carta or Pulley, expense management on Ramp, Brex, or Bill, and reporting that pulls from Salesforce or HubSpot for pipeline and from product instrumentation for usage.

A fractional CFO who is not comfortable in this stack will burn limited, expensive hours learning the tools instead of running the function. With part-time hours, that ramp tax is even more costly than it would be for a full-time hire.

The check: ask which of these tools they have used as the operator, not as an observer. There is a meaningful difference between a CFO who built the close in NetSuite themselves and one who reviewed reports their team built.

6. The Right-Sizing Instinct

This is the attribute that separates a good fractional CFO from a good full-time one. A fractional CFO has limited hours and serves more than one company, which means the entire value of the engagement depends on aiming those hours at the work that moves the business and operating through your existing team rather than trying to do everything personally.

The right fractional CFO walks in and quickly sorts what only a CFO can do, the metrics architecture, the model, the board narrative, the capital strategy, from what your bookkeeper or controller can own with direction. They build the systems and the cadence so the function runs between their sessions, instead of becoming a bottleneck the company waits on. The wrong one tries to act like a full-time CFO at part-time hours, spreads thin, and leaves the high-value work half-done.

The check: ask the candidate how they would spend their first month and where they would deliberately not spend time given limited hours. A strong answer is specific about what they would own, what they would push to your existing team, and what they would leave alone for now.

Talk to a CFO

If you are running a growing SaaS company off a bookkeeper and your own instincts, and the board questions are starting to outrun what you can confidently answer, a short conversation with an experienced SaaS fractional CFO is worth more than another quarter of guessing. It will tell you what is actually missing in your finance function and whether fractional is the right shape for where you are.

Book a CFO strategy call with Ascent CFO Solutions and get a clear read on what your SaaS finance function needs.

Get right-sized financial leadership from experienced CFOs ready to lead your team.

Mistakes Founders Make When Hiring a Fractional CFO

A few patterns come up repeatedly and are worth naming.

Hiring for industry breadth instead of SaaS depth. A fractional CFO who has worked across services, manufacturing, and consumer products may be excellent in the abstract and still struggle inside a SaaS P&L, because the metrics, the rev rec, and the cadence are all different. With limited hours, there is no time to absorb SaaS on your dime. Depth in SaaS specifically beats breadth across the board.

Hiring a part-time bookkeeper and calling it a CFO. The market is full of part-time finance help at a wide range of seniority. A senior bookkeeper or an accounting manager working a few hours a week is not a fractional CFO, even if the title gets used loosely. If the person cannot own the metrics architecture, the model, and the board narrative, you have hired bookkeeping support, not financial leadership, and the board questions will still go unanswered.

Underspecifying the engagement. A fractional CFO needs a clear scope: what they own, what your existing finance staff owns, what you retain, how many hours or days the engagement runs, and what the deliverables and cadence are. Without that, a part-time engagement drifts, the hours get consumed by whatever is loudest that week, and the high-value work never gets done.

Waiting for a crisis to bring one in. Founders often wait until a raise is imminent or a board has lost patience before adding a fractional CFO, which means the foundational work, clean metrics, a defensible model, investor-grade reporting, gets done under pressure instead of ahead of time. The highest-value version of a fractional CFO is the one who built the financial foundation before you needed to lean on it.

What the First 90 Days Should Look Like

A well-run SaaS fractional CFO engagement has a recognizable shape, though unlike an interim engagement it builds toward an ongoing rhythm rather than a handoff.

Days 1 to 30 are orientation and quick wins. The fractional CFO learns the business and the contract patterns, gets the core SaaS metrics calculated correctly and consistently, assesses the model and the close, and fixes the most visible gaps, often the metrics that were not board-ready and the rev rec that was not holding up.

Days 30 to 60 are establishing cadence. The monthly reporting package takes shape, the forecast gets onto a regular update rhythm, board materials get built or sharpened, and the working relationship with your existing finance staff settles into who owns what. The function starts running on a predictable beat.

Days 60 to 90 are the operating rhythm taking hold. The close, the forecast, the metrics, and the board cadence run reliably on the fractional CFO’s leadership and your team’s day-to-day work. The forward-looking conversations, capital strategy, scenario planning, the questions that come before big decisions, become a regular part of how you run the company rather than a scramble. From here the engagement is ongoing, scaling up around events like a raise and settling back during steady stretches.

If a fractional CFO engagement does not have this shape by day 90, with the metrics defensible, the cadence established, and the high-value work owned, the engagement is not running well.

FAQs About Fractional CFOs for SaaS Companies

1. How quickly can a SaaS fractional CFO ramp up?

A senior fractional CFO with deep SaaS experience is typically useful within the first few sessions and has the core metrics, the model, and the reporting cadence in shape within the first month or two. Because the hours are limited, the ramp is measured in the right priorities being addressed quickly rather than in full-time weeks. A candidate who would need a full quarter just to get oriented is the wrong fit for part-time SaaS work.

2. How many hours does a fractional CFO actually work, and what does it cost?

It varies with the stage and what is happening, commonly ranging from a few days a month for a steady-state company to a couple of days a week around a raise or a board push. Cost typically lands somewhere in the range of $5,000 to $12,000 a month depending on scope and intensity, against $250,000-plus in total compensation for a full-time SaaS CFO. The model exists so a company doing a few million in ARR can get real CFO leadership without a full-time salary.

3. How is a fractional CFO different from an interim CFO?

A fractional CFO works part-time on an ongoing basis, often across more than one company, and is the right model when you need consistent CFO-level thinking but cannot justify a full-time hire. An interim CFO works full-time for a defined window, usually three to nine months, and is the right model when you have lost your CFO or need concentrated coverage through a transition. Fractional is part-time and ongoing; interim is full-time and time-bound.

4. When do we graduate from a fractional CFO to a full-time one?

Usually when the volume and complexity of the financial work genuinely require full-time attention, which often arrives somewhere past $20M to $30M in ARR, or sooner if you are moving through back-to-back transactions or scaling unusually fast. A good fractional CFO will tell you when you are approaching that line and can help define and evaluate the full-time hire. Until then, paying for full-time when you need part-time is cost without return.

5. Can a fractional CFO really own our metrics and board work part-time?

Yes, when they are genuinely senior and the engagement is scoped right. The metrics architecture, the model, and the board narrative are CFO-level work measured in expertise and judgment, not raw hours. A senior SaaS fractional CFO who has built these before can establish them and keep them current on a part-time cadence, operating through your existing finance staff for the day-to-day. The key is hiring real seniority and giving the engagement a clear scope.

The Right Fractional CFO Answers the Questions Before the Board Asks

The SaaS companies that handle growth well are the ones that put senior, SaaS-experienced financial leadership in place before the board questions started outrunning their answers, scoped the engagement clearly, and used the fractional model to get CFO-level discipline without a full-time cost they could not yet justify. The metrics got calculated correctly, the model became defensible, and the board conversations stopped being a scramble.

We help SaaS founders and CEOs in Boulder, Denver, and across the country build investor-grade finance functions with experienced fractional leaders who have run finance at venture-backed and PE-backed SaaS companies. Through our fractional CFO services, we own the metrics, the model, the rev rec, and the board cadence on the days your business needs it, and scale up when a raise or a transaction calls for more.

Book a CFO strategy call with Ascent CFO Solutions and put the right SaaS financial leadership in place before the next board meeting.