Ascent CFO Solutions is excited to share a highlight video + full recording of our 2023 Denver Startup Week Session – Ask a Fractional CFO: Ascend to Your Next Stage of Growth!

In this session, experienced Fractional CFOs discuss how their role helps entrepreneurs build sustainable businesses that are ready for their next stage of growth. These seasoned financial professionals have been in the trenches with founders and all types of startup companies through key stages of transformation, including those that are pre-revenue, bootstrapped, private-equity and venture capital-backed.

One such entrepreneur is Caroline Creidenberg, founder of Wedfuly. She shares her insightful experiences of pivoting her business model, leading her team through rapid growth, pitching on Shark Tank, ultimately selling her company, and what knowledge was required along the way.

Founders leave the session with a deeper understanding of how both a Fractional CFO and a firm understanding of their financials can help them reach their growth goals.

Highlight Video

Enjoy this 6-minute highlight reel of some “best moments” from the one-hour session.

Full Session Recording + Outline

Reference the outline below to navigate to the parts that interest you most!

16:00 – Background on Ascent CFO Solutions & how we help entrepreneurs grow businesses.

20:00 – Maris LicisandJodi Mercer share the unique joys and challenges of being a Fractional CFO and why they love what they do.

26:00 – What it’s like for entrepreneurs to work with a Fractional CFO.

— Q&A —

31:00 – How is it helpful to bring in a Fractional CFO when you’re actively raising or looking to raise capital?

32:30 – How do Fractional CFOs work with companies through the different stages of growth?

37:00 – How Fractional CFOs help bootstrapped and early-stage companies bulletproof their pitch decks.

39:00 – How do you integrate fullywith the client’s team?

42:15 – What trigger do you look for that tells you it’s time to move from cash to accrual-based accounting?

43:45 – Do you match a Fractional CFO to a company’s industry?

48:30 – Do you work with nonprofits in the grant writing phase?

49:00 – When does it make sense to have a full-time CFO?

51:30 – When is the right time for an early-stage company to bring in a Fractional CFO?

53:30 – What growth-stage businesses might look for when considering buy-side M&A opportunities.

55:45 – How do you work with banks, either for debt or equity?

58:30 – The benefits of problem-solving with your Fractional CFO.

What other questions do you have about working with a Fractional CFO?

Ascent CFO Solutions is a Fractional CFO firm offering outsourced Fractional CFO and Interim CFO services, financial modeling, M&A, fundraising support, and robust data visualization solutions to high-growth start-up and scale-up companies. We welcome a no-obligation conversation to discuss your business needs.

As a Fractional CFO, I am always looking for ways to increase my efficiency and effectiveness in advising companies on their financial strategy. Staying on top of trends, the economic environment, and gathering and analyzing data are a large part of my role to ensure I’m making the best recommendations for my client’s business. Technology helps with this in many ways, and its capabilities are increasing rapidly.

We are entering a new era where artificial intelligence (AI) is accelerating how efficient each of us can be. In the very near future, AI tools are going to be just as critical to all of our roles as a Google search. In today’s modern era, proficiency in utilizing Google is essential for efficiency. Likewise, lacking expertise in AI tools will hinder your ability to access information quickly and make informed decisions.

As CFOs and executives, it’s essential that we learn how to interact with AI effectively. In this article, I discuss where AI is now, where AI could be going in the future, and how you can be using AI to increase your efficiency right now.

Where AI is now – and why we’re hearing so much about it.

AI is a basket of technologies that do different things. What they have in common is that they take vast data sets of information and layer on top an interface that allows us to interact with it.

Level 1 of AI was all about the robots. Known as Traditional AI or Robot Process Automation (RPA), level 1 of AI recognizes patterns in mass amounts of data, classifies data, and makes predictions. It’s commonly found in a lot of software tools. It analyzes data and executes the tasks that it’s programmed to do. For example, there are finance and accounting tools that intelligently sort transactions, create expense reports, reconcile accounts, and more.

Now we’re in Level 2 – where AI feels a lot more human. Through Generative AI tools, like Open AI’s ChatGPT, we can talk to AI in a natural, conversational way. Based on the context and content it’s trained on, it produces entirely new content. The most prominent version is text, but there is also AI that is generating graphic design, photo-realistic pictures, audio, and more. Mid Journey, Dall-E, and Jasper AI are a few additional examples.

The natural language format of these “Level 2” AI tools makes AI accessible to everyone, and it allows us to process and create content with a level of speed and efficiency that wasn’t available before.

Where AI is going – and what AI means for our roles as finance professionals and executives.

One of the things that’s critical with AI technology is understanding how it impacts our roles as executives, CFOs and financial professionals.

The way I see it, AI is another tool at our disposal that helps us sift through large amounts of information. As CFOs, for example, we are constantly dealing with large sets of data. We take in as much information as possible, look for patterns, and provide value by turning data into actionable intelligence that we can provide leadership teams. We combine it with our own skills and knowledge to make the best possible recommendations that we can. AI speeds up that process, allows us to digest even larger amounts of data, and makes us more effective.

It will soon become indisputable that each individual must possess the knowledge of effectively leveraging AI to stay abreast with the pace of business in our respective roles. However, we are still far from the point where AI can replace our positions, particularly at the CFO and executive levels. Will there be portions of our roles that AI will take over? Yes, we’ve already seen this at the administration level. AI will free us up to work on higher-level strategic work (and do that work faster). However, human intervention will always be necessary in leading and executing a company’s finance and accounting functions.

AI is powerful, but it doesn’t fully consider the human element. AI can generate unexpected and inaccurate results (sometimes referred to as “hallucinations”). Additionally, it lacks the understanding of human intuition and how that might change the relevance of the results.

Instead of expecting AI to replace the finance and accounting function in the future, it is more advantageous for companies to consider engaging with a highly effective and efficient Fractional CFO who utilizes the best tools available such as AI. While many organizations likely don’t require a full-time CFO, there will always be a need for someone to analyze the quantitative results from the AI, provide their unique industry expertise and knowledge, and make a fully informed recommendation.

How CFOs and executives can start using AI to be more effective right now.

AI is extremely useful for a CFO or executive whose time is very limited. As I mentioned, I am a Fractional CFO who works with several businesses advising them on financial strategy and execution. My focus is on working with tech startups, and I’m very passionate about technology as well as finance. Here are some recommendations based on how I’ve been using Open AI’s ChatGPT in my own daily workflows.

1. Researching and Summarizing Information

ChatGPT is an incredible tool for busy CFOs and executives who need to research a lot of information, are responsible for condensing a complicated topic for a client or team, or want to boost the amount of content they absorb–quickly and effectively.

Use ChatGPT to:

Paste in a link to an article and ask ChatGPT to give you a summary.

Engage in a conversation about those points or summary.

Tell it who you want it to respond as/to, and see how it is able to tailor content directly to your use-case. The more context you give it, the more powerful it becomes.

Example prompts to ask ChatGPT:

“Can you summarize the top 3 points of this article?”

“Provide a 300-word summary of this article.”

“Tell me more about what it said on [this topic].”

“Boil down this information using a viewpoint of a CFO with 25 years of experience.”

“From the viewpoint of a novice, or someone who doesn’t understand finance, tell me why inflation is bad for people.”

With a Google search, we all learned how to use keywords and search terms. With AI, it’s now about learning how to use prompts. You can ask it questions or ask it to create something for you, but it takes practice and experimentation to figure out how to craft effective prompts so that it gives you responses tailored to exactly what you’re looking for.

2. Creating New Content

CFOs and executives can use AI to help drive the creation process and drive it faster. Within seconds AI will feed you ideas, then you can iterate on those ideas.

Drafting Documents and Presentations

Finance and accounting professionals tend to be more numbers focused, however, CEOs and leadership teams need to make sense of a lot of information, and it’s on us as CFOs to present that information in a more creative fashion. We can use AI to create content that can be utilized by a company to inform better decision making.

AI can help us generate and improve content for:

Pitch deck presentations

Business plans

Written narratives for financial analysis

Example prompts to ask ChatGPT:

“Create an outline for a pitch deck soliciting funds from angel investors for a small tech startup in the SaaS industry.”

“Draft a business plan for an e-commerce startup with 3 different lines of businesses.”

“This is a pitch for an e-commerce startup. I’m talking to VCs to ask for series A investment. I need help in this section. Generate content around ___.”

“In the style of this pitch deck, help me generate a pitch deck that’s similar to that for this type of company seeking this amount of funds.”

“I’m writing a financial analysis to explain our company’s performance to the company’s board of directors. Help me make it more succinct.”

You’ll have to iterate on this content, give it parameters and more information, check for accuracy, and battle test it (more on that below), but you can use it to create something unique and interesting faster than you would’ve been able to alone. For highly complex tasks and analysis, try breaking it down into small sections and iterate through those pieces.

Excel Sheets & Coding

For executives, CFOs, or accounting professionals who are using Excel frequently or digging into code occasionally, there are instances where you can collaborate with ChatGPT to increase your efficiency. It can correct your mistakes, give you formulas, and simplify your logic. It can debug javascript, python, HTML and explain what the code does, giving you the opportunity to fix it or understand it yourself before engaging with developers.

Example prompts to ask ChatGPT:

“What’s wrong with this formula?”

“I’m trying to ___. What’s a good formula for this?

“Is there a more condensed way to come up with the same logic?”

“Explain to me what this code does and how it does it as if I’m a financial professional with a very base-level of coding knowledge.”

On occasion, we may overlook the distinction between two apostrophes and a single quotation mark, but ChatGPT is able to identify such errors. While pivot tables and v-lookups demand a specific format, the index function offers flexibility to search anywhere in your data. Although many people are not well-acquainted with the index function, ChatGPT can guide you on when and how to utilize it. By describing your data and objectives to ChatGPT, you’ll undoubtedly witness a significant acceleration in your creative process.

It’s a game-changing technology, but that being said, it’s not 100% there yet.

Right now, ChatGPT is still very confident even when it’s wrong. It will occasionally make up something because it wants to try to engage with us. For that reason, we should not consider it an authoritative source, but I anticipate that may change in the very near future. ChatGPT launched in November 2022 and it was already on version 4 as of March 2023. It’s improving exponentially every week. Based on my experiences, its results are approaching 90-95% correct based on the data sets that it has. It’s gotten iteratively better in an insanely fast amount of time.

My recommendation is to “battle test” your results. Start by asking questions you already know the answer to. That way, you can gain confidence in what it can and can’t do. For questions you don’t know the answer to, check the results for accuracy. You can ask ChatGPT to provide its sources so you know what information it’s pulling and can verify it. There is an early-stage API interface that allows you to add and analyze your own data as well.

In the hands of a professional, ChatGPT can help boost your efficiency when doing analysis, making recommendations, and helping customers and clients make better decisions.

The best thing an executive or finance professional can do is dig in!

My primary recommendation is that we all start becoming comfortable with AI now. AI is not going away; it’s only going to accelerate. It’s incumbent upon all of us in the profession to get used to building prompts and asking really good questions in a way that AI can return something to us of value. Chat-based AI tools and prompts are the leading AI interface, so this skill is key.

We’re early on in the emergence of AI, but this is happening quickly. Start trying it out. Get used to the interfaces and functionality, and get a feel for how to leverage it. Create free accounts, experiment, battle-test it, and talk to people about how they’re using it and what they’ve learned.

If you want to exchange stories and insights, connect with me on LinkedIn. I’ll look forward to hearing from you! If you’re interested in learning more about how a Fractional CFO can help your company reach its next stage of growth,connect with Ascent CFO Solutions.

Financial literacy is imperative for all business owners and executives, especially as they navigate a changing and uncertain environment. In honor of Financial Literacy Month, here are a few of our top tips for increasing your financial literacy in your company:

Study your cash flow cycles. Observe and understand the inflows and outflows of cash in your business each month. This is the financial lifeblood of your company.

Establish reliable accounting systems so you know the numbers you’re looking at are accurate. It’s 100% necessary for your business’ success. Rely on accounting professionals to set it up for you, but challenge yourself to understand how the systems work.

Familiarize yourself with a rolling forecast. It projects your future financial scenario based on historical data and what you are predicting about future pipeline and costs. It’s one of the most powerful financial tools you can have. A Fractional CFO can build it for you and provide strategic insights.

Find a CFO, Fractional or full-time, who helps you make sense of your business from a numbers perspective, is educational in their approach, and serves as a strategic advisor to you and your leadership team. Ask plenty of questions.

Invest in a modern data visualization solution. Excel can be overwhelming, clunky, and fragile. There are more robust solutions out there now. Ask us for a recommendation!

Ascent CFO Solutions is a team of diverse and talented financial professionals. In this series, we will spotlight team members to highlight the unique talents and experiences that each one brings to the table for our firm and clients. First up is Carol Wood, a Fractional CFO with a career focus on helping technology companies scale to their next level of growth. We are thrilled to introduce you to Carol, and we hope you enjoy learning more about her.

Did you always know you wanted to be a (Fractional) CFO when you grew up? How did you get started in finance and accounting?

“In some ways, yes! When I was little, my aunt gave me voided checks so I could play ‘business’. I remember seeing everyone carrying briefcases around, and I wanted one too.

As I got older, my father encouraged me to pick a major where I would get a stable job out of school. With my aptitude for working with numbers and since I liked the idea of being in a business environment, it led me to pursue accounting.

I started my career in public accounting, and after working in several industries, I developed a passion for the technology industry. There are always so many exciting things going on in tech, and I’ve been fortunate to work with some really great companies.”

Speaking of those great companies, you were the CFO of Intrado, Freshwater Software, PaySimple, and Dizzion, all of which had successful private equity or strategic exits.What did these experiences teach you? What do successful exits have in common?

“It’s inspiring to work with entrepreneurs who have big ideas and take big risks to bring them to life. They’re investing their own money, taking investment money from friends, family, and shareholders, and they’re putting their necks on the line to grow their businesses.

I’ve seen the hard work that goes into growing a business, and I’ve been through the ups and downs with these teams. Every company has its waves and has to pivot at some point. It requires adjustments and immense perseverance to get to an exit. It’s so rewarding to see entrepreneurs succeed, along with their teams who contribute their sweat and tears and their investors who took risks with their capital. There are so many pieces that go into it, and it’s very exciting to be a part of a successful outcome.

What all of these companies had in common was perseverance and the ability to be flexible and go through change. Along the way, there were times to invest and take risks, and other times when they needed to pull back. The team and the people are key. It’s important to have a team that’s really dedicated and committed to the journey.”

You also have a lot of experience in fundraising and VC. Tell us about it.

“In my previous roles, I have been the ‘VC-person’ that a company hires when they’re raising their Series A. As the CFO, I help them get their financial operations and strategy in order to prepare them for the next level of funding. This also helps position companies for an exit, whether it’s through private equity, a merger or acquisition, or an IPO. I typically stay with a company from $2-$40 million, help them get to that transition, then it’s time for me to go and do it again.”

Why did you become a Fractional CFO (as opposed to staying a full-time CFO)?

“Initially, I was very attracted to the work-life balance piece of it. I love that I’m able to travel and work from anywhere while engaging with multiple early stage companies.

Being a Fractional CFO allows me to stay a little more high level and not be quite as much in the weeds, and I enjoy being able to see a broad range of companies. Every team approaches their business differently–management styles, business strategies, you name it–and there are opportunities to learn from each company I work with. Two of my clients run on EOS (“Entrepreneurial Operating System”), so I am learning all about that now. Even in this stage of my career, there is still plenty of learning to do.

My passion is helping early stage companies get to their next level, and my skills are really aligned for that type of situation. At Ascent CFO Solutions, I love that we have a strong base of technology clients that I am able to work with as a Fractional CFO.”

Why did you ultimately choose to bring your talents to Ascent CFO Solutions?

“Ascent CFO Solutions has a culture that I really resonate with. It’s hard to put into words. When I was interviewing with Ascent CFO, I liked that I was talking directly to the founder of the company. Dan was very thoughtful in making sure I was the right fit for Ascent and that Ascent was the right fit for me. That was very important to me. I like Dan’s approach toward growing the company and investing in building a supportive culture. I like that we have all-hands team meetings, a Christmas party, and other social events throughout the year.

Most of all, there’s just something special about the people that he is hiring. He’s attracting people that fit the culture, and they’re people that I really enjoy working with.”

You’ve mentioned that your passion is contributing your accounting and finance expertise to help early-stage companies.What are some of the first things you do when you’re guiding an early-stage company through growth?

“Financial modeling is the first thing, and making sure the company is adequately capitalized. When we understand where the inflection points are, we know when the company will need additional capital and we can plan for that.

I also focus on creating a smooth financial operation function. I’ve received a lot of positive feedback in my career about this. The companies I’ve worked with can get through an audit without any problems. I focus on creating the right processes and controls. When you get a smooth financial operation going, it allows you to scale. It’s all about getting the right systems in place for ownership and equity management, payroll, HR, possibly upgrading the ERP system, and so on.

Another important element is guiding and building the team. I interact with my peers on the leadership team to make sure we’re all working together and rowing in the same direction. I help them strategize and put the building blocks in place to get to where we want to be. In building the accounting teams, I enjoy mentoring and elevating those people to succeed within their roles at the company and in their careers.”

You have run nine marathons and numerous half marathons, triathlons, and other races. (Wow!) What has training and running in these endurance races taught you?

“Perseverance. Things get hard at times. I know that if I keep going and have that mindset that I will push through it, it will get better. The satisfaction at the end is worth pushing through the challenge.”

What’s something about you that not many people know?

“If I wasn’t an accountant, I would be a veterinarian. I love animals, and I pursue volunteer opportunities where I can help them. I volunteer at the Denver Dumb Friends League every Thursday morning. I went to Africa last year to vaccinate dogs, cats, and donkeys, and I’m planning to go back later this year. Currently, I am fostering a very sweet dog. I’m focusing on helping her gain some weight and nourishing her into a healthy lifestyle so that someone can adopt her. That is another reason I am grateful to be a Fractional CFO–it gives me the flexibility to devote time to pursuing these additional passions of mine.”

~~~

Ascent CFO Solutions is a Fractional CFO firm giving high-growth startups and established companies the custom financial strategy and execution they need to grow. Learn more about us here.

Year-end planning is imperative for all businesses, especially as they navigate a changing and uncertain business environment. Over the last six months, rising inflation and a likely recession has created fear and panic for some companies as they look to 2023. While business leaders have little control over macroeconomic cycles, they do have the ability to truly understand the specific components of their business, adjust and be flexible in their goals and spending, and navigate uncertainty with greater confidence.

Ascent CFO Solutions’ Founder and Fractional CFO Dan DeGolier shares his insights on how businesses can take advantage of year-end planning and forecasting, how to handle financial uncertainty, and ways to elevate your business for greater success in 2023.

What is Ascent CFO Solutions seeing now as we enter the final month of the year?

“CEOs and companies are still reaching out to Ascent CFO Solutions for guidance and assistance with Fractional CFO needs to help them grow, but there is a level of uncertainty in the business environment now that wasn’t present a year ago.

With the threat of recession looming, increased uncertainty has led to a decrease in revenue growth and fundraising valuations. Some deals are taking longer to close, and there have been major layoffs in the tech space (by now we have all seen the news about Facebook).

While this could sound negative and worrisome for many, the uncertainty has pushed CEOs and leaders to look deeper into their businesses.

They are evaluating their company’s current financial standings, taking more time to really understand their cash flow, relying on us to help them set up robust forecasts, and using all of this knowledge to inform their 2023 goals.”

What can CEOs and founders do to address their concerns about financial uncertainty in the new year?

“First, understand that this is not the time to panic. It’s time to be in tune with your business and how it functions. I have seen many CEOs and companies come into the end of the year with a little extra stress on their plate, and sometimes ambivalence about the next steps to take. Rather than give into the fear, take the time to really double down and make space in your end-of-year planning to evaluate, assess, and develop an action plan.

Spend time understanding your cash flow cycles and finetune your visibility into your company’s cash flow for the upcoming quarters. Take time to understand your collection cycles and payable cycles, and assess your current debt and capital.

Companies need to be aware of how much cash they have and how fast they are burning it so they can understand how quickly they can grow. Even a company that is profitable must watch its cash flow closely, and that’s true in any economic environment. Cash flow determines how many new employees you can hire, how much you can increase base and incentive compensation, whether or not you need to adjust your marketing budget, and more.

Plugging your financial and operational data into one comprehensive data visualization solution can give you access to information and insights with greater visibility and efficiency. Ascent CFO Solutions is excited to be launching data visualization solutions for businesses–ask us about it if that’s something you’re interested in!

For business owners, having a really good forecast, encompassing financials and operational logistics, is key to setting your business up for success now and in the new year.”

What is forecasting and how can it be used to help your business?

“Forecasting gives you a month-by-month view of the likely scenarios of your cash flows. Most businesses use either Excel or a more modern visualization solution like Ascent CFO Solutions’ implements to create and view their financial forecasts. It allows a company and its team members to better assess their current financial situation and make key decisions for the future.”

Budgeting vs. Forecasting—When do you need one or the other?

”The annual budget is a static forecast at a particular point in time, with management and board members signing off on it annually.

For many companies, having a budget makes sense, but the reality is that it may become obsolete. As you enter 2023 and you see what’s happening with your revenue, your pipeline, and your client behavior, you and your team may decide that a rolling forecast is more useful. The rolling forecast considers the information and data you’ve learned as the year goes on and allows for adjustments accordingly. What makes a rolling forecast more ideal for some CEOs and companies is that it’s being updated periodically throughout the year as your business changes.

I’ve always considered a rolling financial model forecast to be one of the most valuable tools available to management. If revenue starts to go in a direction other than what you budgeted for, the rolling forecast can offer scenarios on where to cut costs, pause growth, and save cash. Updating your rolling forecast every quarter or even monthly with actual financial results gives you more visibility into what your future financial scenario is going to look like.”

How can you utilize your rolling forecast to preserve cash?

“For most companies, the two primary areas where you can make mid-year adjustments are headcount and discretionary spending such as marketing spending.

Examine your marketing budget–are you getting ROI from your marketing partners? If your business frequents trade shows, perhaps you send fewer people or opt for a smaller booth size.

You can also freeze hiring and salary increases or even let employees go to preserve cash. Although letting go of employees can be emotional and often difficult, sometimes it may be necessary to maintain a positive cash flow or decrease your monthly burn rate. If you’re a capital-intensive company, like a manufacturer, then capital expenditures (CapEx) are another lever you can pull.

Since companies cannot easily make significant changes to things like benefits packages or real estate occupancy, cutting these discretionary areas is often the fastest way to make an impact on your bottom line.

It is very worthwhile to get lean and efficient with costs when you are trying to preserve cash. See if you can renegotiate your real estate lease(s) to get a price break. The pandemic showed us a perfect example of this in the real estate market as individuals advocated for and obtained lease cuts. Look at your spending. Review your recurring subscriptions to see if you can cut your fixed monthly costs. I highly recommend Cledara as a tool to help companies evaluate and manage their spending on SaaS subscriptions.

Every business is different, and you should have a firm understanding of your current financial situation before making these changes. Stay agile in your finance and accounting operations and rely on your rolling forecast to help guide you.”

What does agility look like in finance and accounting?

“Agility in finance and accounting is about having visibility into your business so you know when to act. It’s about managing your balance sheet, managing your payables, not letting receivables fall too far behind, managing credit limits and policies, and keeping up with client communication to make sure you’re getting paid.

Stay on top of bank debt or bank covenants if you have them. If you think you might miss a bank covenant, alert the bank in advance. The key is don’t surprise your board, investors, or bankers! The better your forecasting, the better visibility in your future balance sheet, and that will help you ask forgiveness before you’ve already fallen into default.

It’s important to take a hard look at your business and where you can make adjustments or cuts. Review your company’s sales organization and cost structure—are you pricing things appropriately? Can you increase certain offerings to customers to increase revenue?

Truly the best advice I can give is to have a good plan and a good forecast to help shape it.”

How can a Fractional CFO help you stay agile and effectively navigate change?

“Many companies can benefit from bringing on a Fractional CFO either part-time or interim full-time. This individual is highly experienced, has likely been through a recession before, and is prepared to make difficult choices.

A Fractional CFO can help you answer questions like:

How much cash do we need to execute on our plan?

Do I have enough cash to grow?

Is our line of credit big enough?

Am I paying people appropriately, and am I going to be able to retain them?

Am I incentivizing my team properly?

If you have a Controller in your company who wants to level up, it may be beneficial to bring on a Fractional CFO as a coach and mentor. A Fractional CFO may be able to provide oversight and mentorship, as well as handle aspects like negotiating with banks or KPI reporting that your current employee may not know how to do.

I encourage CEOs and upper management to consider bringing on a Fractional CFO to streamline their processes and create more efficiency in their day-to-day operations. This could be a game changer for your business in 2023.”

What opportunities can businesses look to take advantage of in 2023?

“There are ripe opportunities for growth for businesses who are prepared to take advantage of them. The recent decline in real estate costs could present an opportunity to buy a building for your company (of course, consult your tax advisor). There may be circumstances to acquire new businesses as competitors may be more motivated to sell. This may lead to a better valuation or a better deal in a merger and acquisition situation. It may also be a good time to accelerate buying equipment because vendors might be offering discounts.”

The Big Takeaway for How to Prepare for 2023

“I urge any CEO or company leader topay attention to the numbers to really know your business. Have a plan B and be ready for a slowdown, so if you need to cut costs, you’re ready to pivot. Pay attention to your sales pipeline, and make sure your team is properly motivated and compensated. And be sure to have good visibility into your future cash flows via a robust rolling forecast.

Be really in tune with your business. Know when to pump the brakes or push forward into new opportunities in 2023.”

As the Software as a Service (SaaS) business model soars in popularity, companies face a big dilemma of how to establish metrics to run the businesses in a manner that maximizes value.

The value of starting a SaaS business is to show investors that there is a large addressable market, a high likelihood of the team being able to execute, and low investment risk due to the amount of base revenue and traction that is recurring. To protect annual recurring revenue (ARR), there are various metrics that management should be measuring. Often companies do not maximize their highest potential because Key Performance Indicators (KPIs) are not established across all departments to measure business activity from the very start.

This article will discuss some of the KPIs that every SaaS company should measure. A management team that only looks at these measurements at a single point in time will miss unlocking their true value. It’s important to track KPIs over time to reveal insightful trends that allow you to see if there is forward or backward progress. A downward trend indicates a decision needs to be made to intervene so it doesn’t create problems in the future. This is the reason it is so important to establish the KPIs from the very beginning. Oftentimes companies find themselves having to look backward in time to try to find and recapture this data, and this causes a lot of wasted time and resources.

Another critical item is establishing the KPIs in the system of record. The ultimate goal is to capture all your data in a CRM system that is linked to the financial system of record. This makes the data easy to present and share with management as well as the entire company. Time and resources are also saved by minimizing the need to create manual spreadsheets that have a larger chance for an error.

The following are the KPIs that all SaaS companies should track:

1. Net Retention – this measures the health of the current customer base. In order to calculate this, you take your current customer base ARR from twelve months ago and compare it to what it is today.

World-class retention is over 110% and tells a management team that most of their customers stay engaged and are actually growing. Growth within existing customers indicates stickiness and customers are more apt to stay engaged over the long term.

If this percentage is under 100, it tells management that they are losing revenue from current customers that were signed up over a year ago instead of growing their portfolio with these customers. This shows adoption is low and customers are lowering the number of licenses or deleting products they no longer need. For additional clarity, think of this as your “organic” ARR growth that needs to exceed your partial churn and your full customer churn in a given year.

Leadership must put resources towards improving the current environment for customers so they sign up for more products or seat licenses. Marketing and sales departments should work together in establishing internal campaigns to attract customers to re-up rather than delete products. They also should put training programs in place for customers to increase their product knowledge of customers.

2. Churn – this measurement tells management how many customers they lose on a yearly basis. There are many ways to calculate churn, but the most effective way is to look at the revenue dollars lost compared to the total ARR of the company twelve months ago. Anything below 5% is world class and anything above 10% creates a red flag for management and investors.

Another important factor in calculating churn is to see the correlation between the churn revenue percentage and the number of churn customers. To calculate the number of churn customers, take the total number of customers twelve months ago compared to how many customers churned during that time. If the results show a high percentage of customers that have churned but the revenue churn is still less than 5% then the problem is not as bad as one would think because the smaller customers are going away.

In this scenario, management may create a program to retain specific customers that are under a certain revenue threshold. However, if the revenue churn is higher than the customer count churn, this is more problematic because the company is losing bigger customers. Leadership needs to focus on that so the trend doesn’t continue.

3.ARR Backlog – If there were no more sales and every customer stayed with the company, this would be the annual recurring revenue that is guaranteed. This is a great measurement for banks and investors that are looking at the company.

To calculate ARR backlog, take the current monthly recurring revenue (MRR) plus any revenue that wasn’t recognized that month because a new deal was signed in that month, less any revenue recognized that month that was ultimately churned during that month, and multiply by 12.

What most investors do is take a churn factor based on trends and then add new business factors to get a reasonable backlog going forward. Trends are very important for this metric because if management sees ARR backlog going down each month then something needs to be done. The new business coming in is not fast enough to offset the churn from existing customers.

There are many sales metrics for new business and existing business customers that also should be looked at when running the SaaS sales organization.

4.New and Existing Bookings – this is the entire amount of the first year of revenue. In SaaS business models, there is usually a one-time, non-recurring revenue (NRR) for implementation services. It’s important to separate the NRR from the MRR because the focus for maximizing value is MRR.

Management should also provide guidance to the sales team on the ratio between MRR and NRR because, in selling, the main goal is to maximize the MRR as that creates future health for the business. The NRR goes away after year one. There also should be discount percentages established upfront because if the sales team continues to discount ARR it may cause issues with creating a high ARR backlog. Companies should incentivize their sales personnel to sell more MRR. It’s amazing the results that are achieved when employee compensation is well aligned with management goals.

5.Stages 1-5 Sales Pipeline – each company should establish parameters for their sales pipeline and put opportunities in the right categories as they reach certain stages of their sales cycle.

This is a key activity because it helps with forecasting. Once you collect a couple of years of data, a company can review each stage of the pipeline and predict the dollar of bookings that will eventually close as well as the length of the sales cycles. This creates predictability and assurance that the goals established at any given time are reasonable. Management also can make decisions on headcount, forecasting, training, etc. if they have good pipeline data to analyze.

Everyone in the company can help establish metrics and hold themselves to achieving maximum MRR.

Office administrators may greet customers by phone and in person and if they are not cordial that customer might churn. The employee in charge of collections has to deal with customers every day and has to try to collect money. Going about it the wrong way could cause a churn. The existing and new business sales teams have to work with marketing in maximizing ARR. The engineering team must make sure the product is up to date so customers don’t get bored and want newer or better technology from competitors. The customer support team answers the phone and has to solve customer issues in a timely manner. The executive team needs to ensure everyone is always on the same page.

It’s very important all of these teams have access to KPI data so decisions can be made promptly and efficiently. Without the KPI information, companies are not able to make these very important decisions timely. It is never too early to start!

Rather than hire a full-time permanent replacement when its first CFO left the company, Josh Freed, founder and CEO of workplace-management software startup Proximity, decided to do something different. The company contracted a fractional CFO, along with other fractional accounting staff, to take over the company’s finance functions.

The move made good business sense: A fractional CFO, kind of a finance freelancer, costs less than a full-time CFO, and their workload is dictated by the company’s needs. And it made good strategic sense for Proximity as well; by offloading daily accounting tasks to part-time accounting staff, the fractional CFO was able to focus deeply on the company’s strategic activities.

The fractional CFO, actively engaged with multiple clients simultaneously, also brought a wealth of outside knowledge and contacts to the company, experience and vision that a full-time CFO might not necessarily have, Freed said.

“We’re able to take a daily eye off of the metrics of the company when it comes to finance, the day-to-day accounting, knowing that once we onboard them, that they have their arms wrapped around certain aspects of the company,” Freed told CFO Brew.

Fully fractional. But fractional CFO work isn’t just beneficial for companies. For finance professionals with an entrepreneurial spirit, fractional CFO roles can be a path to greater flexibility, accelerated career development, and a way to broaden and diversify their experience.

Anne Marie Dube wanted a change after spending decades working a variety of finance roles for both large and small organizations without making it to the CFO chair, a long-time career goal. So when a venture-capital firm offered her the chance to work as a fractional CFO at a small firm that needed financial leadership, she leapt at the chance.

That first job led to more work, and Dube is now a fractional CFO for multiple clients and hopeful that one of those gigs leads to a full-time CFO role.

“At this point in my life, I can take a lot of clients, I can get to know the different industries to where I fit in, which one suits me the best,” said Dube. “And then, hopefully, a full time position comes of it.”

Duke Heninger started fractional CFO work much earlier in his career than Dube. After stints in public accounting and in industry, he found himself bored and looking for new opportunities.

“I wasn’t really being challenged, so I jumped out and started doing fractional CFO services,” he said. “At the time, I really thought it was a means to an end.” While working as a fractional CFO, Heninger bought, and recently sold, a business.

“Because I’m fractional and a contractor…it doesn’t matter where I’m at right now,” said Heninger. “I can pursue what I want to pursue and get paid really well for it.”

Stepping in and stepping up.The Wall Street Journal reported last year that the demand for fractional CFOs was on the rise, driven largely by fast-growing startups flush with venture capital and private equity, but weren’t always prepared for the complicated financial matters that an influx of such capital typically brings.

“What we’re seeing more and more is that the small growing companies are blowing up everywhere, especially on the tech side, but also on e-commerce as well. They are needing high-level guidance, but they just can’t afford a $250,000 CFO,” Heninger said.

Although the startup scene is starting to cool, demand is still high for fractional CFOs according to Dan DeGolier, founder of Ascent CFO Solutions, a Colorado-based CFO outsourcing firm.

“It’s expanded very dramatically,” said DeGolier. “There’s definitely been a maturity within the fractional CFO space with the acknowledgement that it’s a really good approach in quite a few different industries for growing firms or firms that are going through transition.”

Not for beginners. To be clear, fractional CFO work is not for entry-level candidates. But for finance professionals with the right accounting, strategic, and soft skills to step into a company and immediately start steering the financial ship, the work offers a range of career benefits.

“You can’t go and just work at a fractional CFO firm from the bottom up,” Heninger said. “You have to have that real-life experience before you can get into it.”

And fractional CFOs are often tasked with more strategic, big-picture work and less with routine accounting and finance processes. For that reason, fractional CFOs often gain a deeper, broader skill set and network than finance professionals staying at one company, according to DeGolier.

“When I’m talking to a potential CFO joining the team, I’m letting them know they’re going to get quite a bit of variety and flexibility by working with several clients, and just doing that higher-level CFO work, it’s almost like putting your career on hyper-growth mode,” he said.—DA

We’ve previously written about exit planning broadly, and about building a perfect pitch deck more specifically. Now, we come to the step of navigating due diligence. This is one of the final steps to get your deal closed whether you are raising Angel/Seed capital, VC funding, or perhaps completing a sale of your entire business. It’s critical for any company to be prepared and organized before due diligence begins to preserve your agreed-upon valuation and not have to accept less desirable terms as a result. Worst case, lack of preparation could result in the deal falling apart.

The good news, even for a first-time fundraiser/seller, is that you are likely familiar with the concept of due diligence and may have performed some of the steps in a personal capacity. Investing in the stock market, for example, requires analyzing company or fund prospects, to determine if they fit within your investment goals. Investors will undertake an amplified version of this process, often hiring professionals to analyze and dig deep into a company’s operations before making a decision to acquire.

In this post, we dive into the mechanics of due diligence, the ramifications for your business, and explain how to prepare for and navigate the process.

What is Due Diligence?

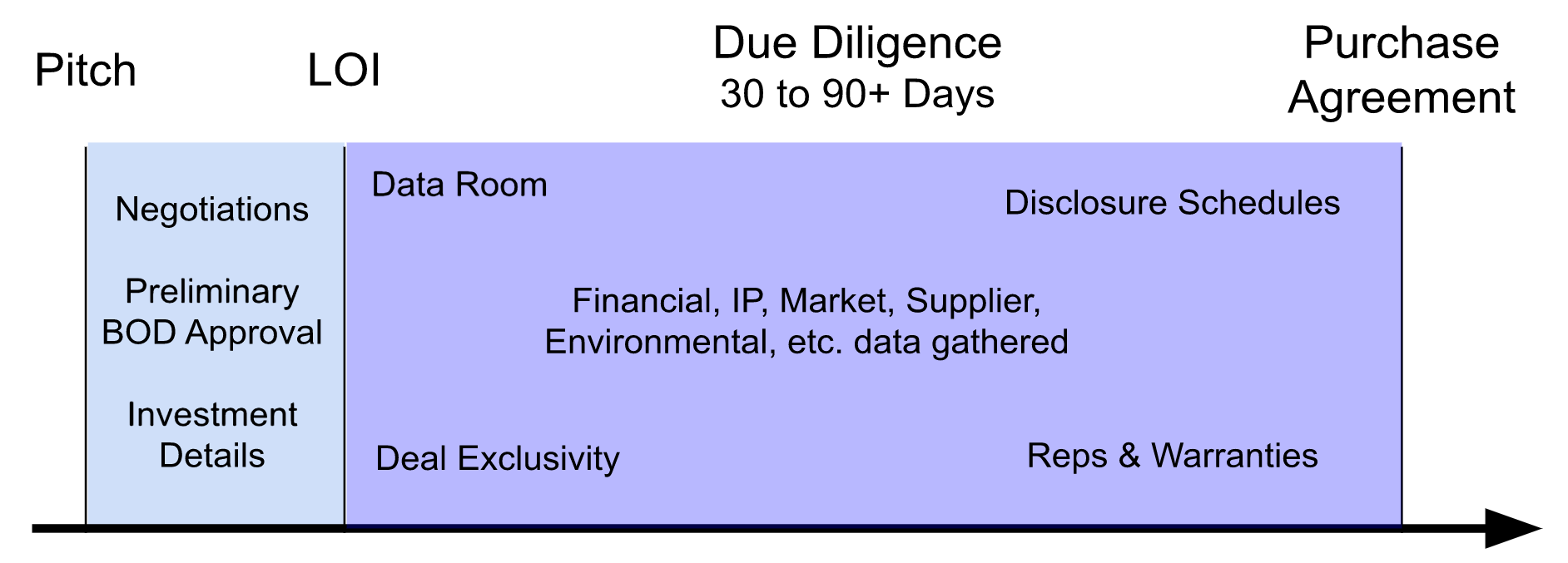

Due diligence is a discovery process in which potential investors or acquirers learn everything they need to determine whether or not a particular company makes sense for their investment portfolio. The process can take anywhere from 30 to 90+ days depending on the scale and complexity of the deal as well as the risk aversion of the buyer.

As illustrated in the example timeline below, due diligence often begins in earnest once you receive a Letter of Intent (LOI), with findings strongly impacting the final deal terms.

We’ll get deep into the details, but for anyone unfamiliar with due diligence it often helps to consider a house buying analogy because the steps of both processes are similar even if the breadth and depth of investigation differ.

Due diligence is most like the inspection phase of buying a house. This is when negotiation occurs as the buyer and seller figure out if the deal is going to work by determining the final valuation and purchase price along with acceptable concessions and warranties.

Types of Due Diligence

In most circumstances, the buyer/investor will direct the due diligence process, and the type of investor greatly impacts the process. For example, a private equity (PE) firm looking to purchase a majority or all of a company is generally going to be more risk-averse than venture capital (VC) or earlier-stage investors. Therefore, they will ask for and review substantially more information.

Understanding the Purchaser’s Perspective

There’s a lot at stake for potential buyers if due diligence fails to uncover serious deficiencies in the company. Not only can a buyer lose their entire investment, but reputational damage could impact future deals and funding. In a stock sale, the buyer inherits the known and unknown liabilities of the acquired company, risking claims or lawsuits from customers, employees, and others that could lead to losses in excess of the actual purchase price.

Due Diligence Categories

Some form of financial due diligence is always a given, but as a business owner, you should also expect data requests and analysis related to:

Technology/IP

Customer/Sales/Suppliers

Material Contracts

Employment/HR

Litigation/Legal

Taxes

Antitrust/Regulatory

Insurance

General Corporate Matters

Environmental Issues

Related Party Transactions

Real estate/Property

Marketing

Competitive Landscape

In the case of PE and VC firms, the investor will coordinate and perform most due diligence activities with their in-house staff, but for specialized tasks, it’s typical for them to outsource tax compliance, quality of earnings (QofE), intellectual property, and IT evaluation to an outside firm.

Not all categories apply to all companies, but being prepared helps ensure a smoother process. For example, if your competitive advantage is the result of a patent, expect to provide information about your intellectual property, steps taken to protect it, and potential challenges maintaining it.

Financial Due Diligence

During financial due diligence, your CFO will take a leading role to discuss assumptions that go into your financial models, the evolution of the competitive landscape, and business opportunities that could be capitalized on with additional funding. The stakes are high because findings directly impact your valuation and deal terms.

Investors will expect to see forecasts for:

Income Statements

Cash Flows

Balance Sheets

They will compare your performance during due diligence with your near term forecasts to look for accuracy and trend changes. There is inherent noise in short term results, so sellers benefit by engaging in relationships with potential acquirers early. Investors that are familiar with your business and financial modeling assumptions can discount that early noise, resulting in fewer surprises and a higher likelihood of a successful close.

Expect investors to focus on different metrics depending on your growth stage. This list below is not exhaustive, nor are the columns mutually exclusive; rather, they serve as an example of metrics investors are likely to value.

Earlier stage, Higher Growth:

Sales & Revenue Growth

Number of Customers & Growth Rate

Gross Margin

Cash Burn

Customer Acquisition Costs (CAC)

Monthly Recurring Revenue (MRR)

Customer Lifetime Value (CLV)

Later stage, Higher Profitability:

EBITDA / Net Income

EBITDA Growth

Discounted Cash Flows

Net Cash/Debt

Book Value

It’s true that investors are looking for red flags, but financial due diligence is also an opportunity to get investors excited about your company’s potential. Your pitch presentations and initial financials are what attracted investors; due diligence is your opportunity to back up those claims and demonstrate that your company is as valuable as your pitch implies.

Working Through Due Diligence

The difficulty of the due diligence process is going to be directly proportional to the operational standards of your business.

For example, a CFO that regularly coordinates with the department leads to establish forecasts, which the company reliably meets, can confidently present these projections to an investor. If you have the appropriate business licenses and maintain accurate records of vendors, ingredients, etc., you won’t need to scramble to gather data on the fly, potentially missing material details on your disclosure schedules.

The idea of continuous due diligence is that the information investors need to determine a valuation is the same data you need to successfully operate your business. For example, a company needs to know if its cash flows support near-term working capital, additional staff for growth, and capital expenditures, so it makes sense to have the data available whether you’re answering an investor question or using the data for internal decision making.

Handling Due Diligence Requests

In many ways, due diligence is a conversation where the investors’ goal is to understand your company, and ultimately, what they’re buying. That conversation starts broad and becomes more detailed depending on previous answers. For example, an investor might ask for an ingredient list if you manufacture a consumable product, which could lead to questions about FDA lists and prop 65 compliance. Other questions are designed to establish trends, like changes in revenue or marketing spend over the course of the sale process.

Sharing Information

When it comes to actually sharing company data, efficiency and security are paramount.

Companies typically opt for an online, permission-restricted “data room” that may take the form of a file share on the company intranet or a third-party service for sharing data securely. A secure data room is beneficial as it limits access to those that strictly require the information which in turn minimizes data leaks and loss of proprietary company documents. Anyone with access should be bound by non-disclosure agreements where appropriate and care must be taken to share only what is absolutely necessary.

An organized, online data room should facilitate quick due diligence request turnaround. Documents can be shared, collaborated on, and updated in real-time keeping the overall deal process on track.

Put the Right People in the Right Places

It is important to establish points of contact and review processes when responding to data requests. Data may be gathered by many individuals, but it usually makes sense to funnel communication through just a few people. Your CFO will communicate with investors on financial matters while your HR designee responds to requests about employment contracts, and so on. This ensures a consistent message from your company to the relevant groups, avoiding confusion and delays.

Finally, controlling points of contact is a good way to have an investor begin to build rapport with the key players in your business and get a feel for the company’s organization.

Impact of Due Diligence

Findings from due diligence make their way into a final purchase agreement in multiple ways:

1. Sale price / valuation

Financial due diligence will bring to light sales trends and profit margins that will inform the sale price. It will be the job of your CFO to accurately convey your company’s financial results and forecasts. Due diligence may also give the buyer reason to request certain reductions in sale price based on findings. For example, a tax audit may uncover $50,000 of unpaid state sales taxes and the buyer, who will soon be responsible for that payment, may request a corresponding sale price reduction.

2. Representations, Warranties, and Disclosure Schedules

Representations (reps) and warranties are the claims that you would assert as true in a purchase agreement. If they’re later found to be untrue, it could result in an indemnification claim to make the buyer whole for any loss incurred. As an example, due diligence may find that your company’s success hinges on a critical patent. In that case, the buyer would ask for a rep asserting that the company does indeed own the patent. It’s also likely to specify the ramifications and compensation owed for violating that rep.

Disclosure Schedules are legal attachments to the purchase agreement in which the seller discloses all relevant information about the business to the buyer. Disclosure schedules list company information such as: key contracts, major suppliers, owned assets, IP, ingredient lists, insurance policies, permits, owned property and assets, employee benefits, shareholders, pending litigation, and so on.

Reps and warranties reference disclosure schedules which give the buyer legal recourse should they suffer damages resulting from untrue seller statements. Disclosures also serve to protect the seller by allowing the buyer to enter into a purchase agreement with full knowledge of any potential issues. Thorough disclosure statements take significant time and effort to compile, review, and negotiate, so it is important to begin the process early, expecting subsequent iterations throughout the diligence process.

Impact of due diligence on business operations

The diligence period brings intense scrutiny to business operations as an investor looks for any misalignment between financial forecasts and actual results.

Making significant changes in your business is going to introduce noise in your operating results while investors are looking for any misalignment between your financial forecasts and actual results. For that reason, companies often opt to avoid making material changes (personnel changes, large capital expenditures, etc.) during due diligence. If a change is critical to the business, it may be worth implementing and working through before beginning a sale process.

Also, expect due diligence to take time and effort from your deal team, which can no longer be spent on day-to-day business operations. Not only will your team need to work through diligence requests, but your employees are likely to be distracted by upcoming deal uncertainty. It’s important to proactively communicate expectations and, in some cases, it’s beneficial to offer incentives to key employees to keep them focused on a successful deal close while keeping up with their existing duties.

Due Diligence as a Negotiation Tactic

After receiving an LOI and a deal is agreed to in principle, it’s common to enter into a period of exclusivity where you won’t pursue a deal with other investors.

Exclusivity creates a shift in negotiating power from seller to buyer because due diligence places operational burdens and restrictions on the seller’s company as discussed earlier. It’s common for the offer price to come down based on findings during due diligence, so it is important to pitch to as many potential investors as possible and receive an LOI for a price higher than your desired final sale price.

It’s worth noting, however, that due diligence does offer some opportunities to the seller. Investigating a company takes time and money to hire the appropriate experts and perform analysis. These are sunk costs to the buyer, so that may push marginally skeptical buyers over the edge to a deal close. Naturally, the buyer will attempt to recover these costs by asking for a price reduction based on findings, but the seller is under no obligation to accept those reductions.

It’s critical for the seller to have a backup plan, whether that’s another investor, or being prepared to continue operations as an independent company. Most buyers are happy to acquire a good business at a fair price for a mutually beneficial outcome, but it’s important to maintain negotiating leverage to garner the valuation your company deserves.

Final Thoughts

Many business owners view due diligence as a necessary evil when selling their company or bringing on investors, but it doesn’t have to be. Practicing continuous due diligence keeps you prepared for a sale while enhancing business operations. Up-to-date income statements, cash flow, and balance sheets with corresponding forecasts allow your company to plan for the future.

It often feels like diligence requests and negotiations come down to the wire in any deal, but successful navigation through the process ends with a purchase agreement that marks a new and exciting chapter for you and your company.

You may have heard of financial modeling. You may even know it can be a helpful tool to grow your business. But what does this actually mean? In what ways is a financial model helpful? What are the tangible benefits a financial model can provide? Let’s take a CPG (Consumer Packaged Goods) startup, for example.

Here are four ways a CPG startup can benefit from a good financial model. Even if your company isn’t in the CPG industry, the benefits can still apply to you. Read on!

#1 – A detailed financial model crystallizes the goals of your CPG startup.

“If you don’t know where you’re going, any road will take you there.”

– George Harrison, “Any Road”

It’s good to have a goal. Distribution in 10,000 grocery stores by 2025. 1.5% market share. A $10 million dollar revenue company. Perhaps these are good goals. But perhaps they are not. A financial model helps you test your goal by taking you deeper. How many SKUs will I have in those 10,000 stores? What will the weekly velocity be? What pricing drives the best velocity? Exploring the subcomponents of the goal and doing the math in a financial model helps you develop confidence in the goal.

#2 – The financial model forces you to think about the pesky details.

“There is no magic in magic. It’s all in the details.”

– Walt Disney

Can you believe a blank shipping label costs nearly a dime? Do you know the cost of the glue used for your folding carton? Is the ingredient cost in your cost of goods sold calculated based on a hypothetical quantity at scale, or on the actual quantity you can afford to order today? How much film waste do you have each time you start your wrapper, and how does that affect your cost of goods? Often-missed costs like these quickly eat up the gross margin of your CPG business. A good financial model forces you to consider all the details, whether it relates to cost of goods, credit card processing fees, online retailer marketing fees, other fees (does anyone really know what all those other fees are?), third party logistics fees, and on, and on.

#3 – A good financial forecast tells you if and when your CPG startup will run out of cash.

“Cash, though, is to business as oxygen is to an individual.”

– Warren Buffett

The fear of running out of cash is both common and understandable. Missing payroll or even sweating potentially missing payroll is gut-wrenching. The inability to buy ingredients for next week’s order is incredibly frustrating. If you had known you were going to be short of cash, you could have done something about it, right?

When building your financial model, you will consider the volume and profitability of your sales. In addition, you will consider other cash-related issues such as the timing of customer payments, up-front deposits required by your co-packer or raw material supplier, the quantity of inventory needed, new equipment required, and even how long you can delay the rent payment before the landlord knocks on the door. Armed with a financial model that considers all your sources and uses of cash, you can confidently move through your business seasons.

#4 – The financial model helps others understand the financial story of your business.

“A good financial model is worth a thousand words.”

– Anonymous

You have a terrific product that addresses a market need. You’ve developed strong ongoing customer relationships. All your sales trends point up. It’s time to bring on new investors, key employees, or develop other strategic relationships. “How much cash do you need, and when?” investors ask. “Am I joining a financially viable CPG business?” potential employees and strategic customers and vendors ask.

In lieu of smoke and mirrors, you advance the well-thought-out, comprehensive financial model. “Let me walk you through the financial story of our business…,” you begin. Your financial model tells you about the health and needs of your business, and once you know the story, you can share it.

A financial model won’t guarantee your business’s success. It will, however, give you confidence in your understanding of the future, enable you to make informed business decisions, and give you a tool to share your confidence and knowledge with others.

It’s true that financially-minded and spreadsheet-savvy individuals can tackle a “DIY” financial model in Excel. To create a robust and comprehensive financial model, however, it’s best to rely on an experienced CFO. They can dive deep into your business to thoroughly understand the drivers of your company, then create a powerful, easy-to-use tool that reflects the unique situation of your startup. Then, you can use the model to experiment. A good financial model is built to survive many rounds of changes as you test assumptions and visualize the effects of pulling certain levers in your business (CFOs can certainly help with that, too). You end up with an actionable strategic plan based on solid financial analysis.

For startups, it’s not always reasonable to hire a CFO full-time. Even with a full-time CFO, your company may not have the expertise (or bandwidth) needed to create a robust financial model. Seasoned CFOs are still within reach. CFOs are available on a fractional basis through Ascent CFO Solutions, giving your company a completely custom arrangement for your particular needs. I encourage you to reach out to us here.