How Do We Implement KPIs Without Overwhelming the Team? Simplifying Metrics for Maximum Impact

Key Takeaways

- Start with 3-5 strategically aligned KPIs to maintain clarity and prevent metric overload, ensuring each metric directly supports your business’s core objectives.

- Implement KPIs through a structured 8-step rollout process, including piloting, feedback, and clear definitions, to drive adoption and avoid confusion or resistance.

- Reduce team stress by automating data collection, limiting manual tracking, and establishing simple, regular review rituals—transforming KPIs into actionable decision-making tools rather than administrative burdens.

Harvard Business Review research reveals that poorly designed metrics can actually undermine business performance rather than improve it. Most KPI programs fail not because teams resist data, but because they face too many metrics, too fast, without context. Teams become paralyzed by metric fatigue instead of empowered by clear direction.

The good news is that there’s a better way. Start with 3-5 business-critical KPIs aligned to your growth strategy, implement them through a structured 8-step process, and embed light weekly rituals that drive adoption without stress. This approach transforms metrics from a burden into a competitive advantage.

Partner with Ascent CFO Solutions to design KPI frameworks that drive growth without overwhelming your team.

Choose the Right KPIs for a Growing Business (Without Creating Confusion)

How do we choose the right KPIs for a growing business without creating confusion? The answer lies in strategic discipline and smart constraints. Most teams become overwhelmed by metrics because they skip the focused effort of connecting measurement to strategy. When you anchor KPIs to your core objectives and set clear limits, you create clarity instead of chaos.

Start With Strategy, Not Spreadsheets

Begin by identifying your 1–3 most important strategic objectives for the next 12 months. Then translate each objective into 1–2 company-level KPIs that directly measure progress. Research shows that organizations with tightly aligned KPIs make faster decisions and achieve better outcomes. A Fractional CFO can guide this alignment process, helping you resist the temptation to accommodate every department’s wish list until your core set proves stable and actionable.

Once You’ve Anchored to Strategy, Apply the 5/4 Guardrail Rule

Cap your metrics at 5 KPIs per team and 4 per individual role. This “54 guardrail” prevents context switching and reporting fatigue that undermines adoption. For instance, a sales team might track lead conversion rate, pipeline velocity, and customer acquisition cost, while avoiding secondary metrics like email open rates. When teams track too many metrics, they lose focus on what matters most. Your Data Analytics platform should reinforce this discipline by highlighting only the metrics that drive decisions.

Define Decisions Before Dashboards

For each KPI, specify the exact decisions it will inform, who owns it, the target range, and action thresholds. This prevents “vanity metrics” (impressive-looking numbers that don’t change behavior) from cluttering your dashboard. When you build a finance culture around decision-ready data, teams naturally focus on metrics that move the business forward rather than just filling reports.

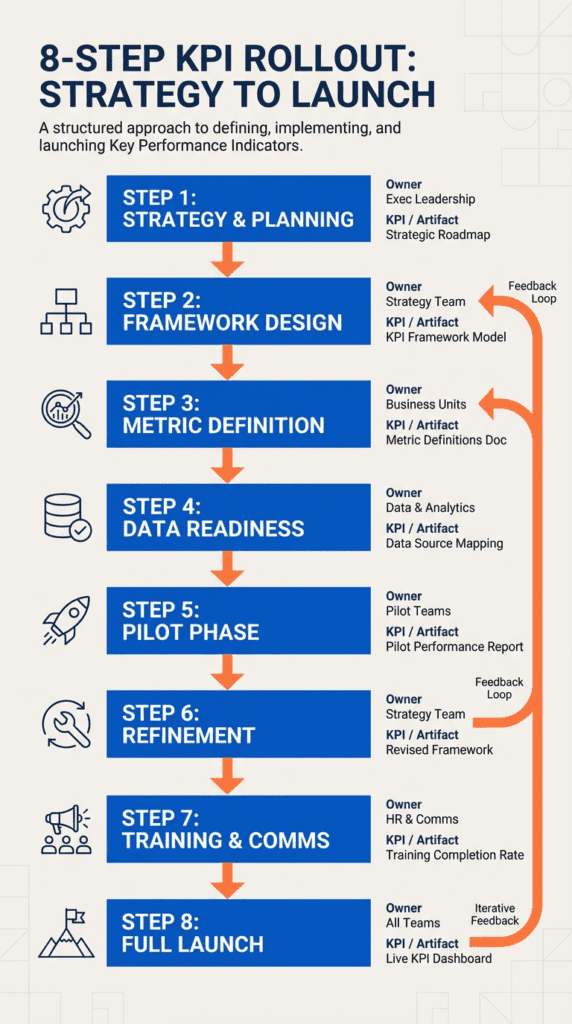

An 8-Step KPI Rollout That Won’t Overwhelm Your Team

Most teams stumble with KPI implementation because they skip steps or try to do everything at once. A structured approach prevents costly rework and builds confidence as you scale.

What are the best practices for introducing KPIs to a small team? Harvard Business Review research confirms that successful pilot projects follow a clear sequence with built-in validation points. Here’s your roadmap:

- Define 1-3 strategic objectives before selecting any metrics to avoid measuring activity instead of outcomes

- Shortlist 3-5 company KPIs using the 5/4 guardrail approach (5 KPIs per team, 4 per role) and resist adding secondary metrics

- Create precise definitions for each KPI including calculation methods, data sources, and target ranges

- Map data sources and validate data quality to confirm reliable, accessible information flows

- Build dashboard prototypes using advanced analytics tools to test usability and visual clarity

- Pilot with 6-8 team members for 2-3 weeks to validate definitions, thresholds, and dashboard functionality

- Collect feedback on clarity, actionability, and time investment before expanding to other teams

- Launch company-wide with established review cadences and clear ownership assignments

This structured approach typically takes 8 weeks with weekly checkpoints to maintain momentum. Teams that skip the pilot phase often face resistance and confusion during full rollout.

Reduce Stress With Lightweight Tracking and Clear Rituals

How can we ensure KPI tracking does not increase employee stress? The biggest mistake teams make is turning KPI tracking into a time-consuming burden. Research shows that poorly designed electronic monitoring increases employee stress and reduces engagement, but smart implementation focuses on rhythm and automation instead.

The key lies in making metrics become decision-making tools rather than daily administrative tasks. Fractional CFO services often include meeting facilitation and rhythm design to support this approach.

- Schedule 30-minute meetings weekly for team reviews and monthly for cross-functional alignment

- Automate data collection through system integrations rather than manual spreadsheet updates

- Use traffic-light thresholds with single ownership per metric

- Limit manual data entry to under 10 minutes per team member per week

- Assign single next steps with due dates when KPIs hit red thresholds

Effective meeting cadences and automated data analytics transform metrics from stress points into momentum drivers. These focused check-ins become productive strategy sessions rather than reporting obligations.

KPI Implementation FAQs for Startup and Scale-Up Teams

Growing companies face predictable challenges when rolling out performance metrics. Teams worry about data overload, conflicting definitions, and metrics that don’t reflect real business value. These answers address the most common roadblocks we see when helping scale-ups build sustainable measurement systems.

How do we prevent KPI sprawl as we add new products and markets?

Lock in your core metrics before expanding into new areas. Each new product or market should inherit the same 3-5 company-level KPIs, then add only 1-2 segment-specific metrics. Research shows that performance indicator selection works best when teams define clear aims first, then limit measures to strategic, actionable metrics.

What’s the best way to align finance, product, and sales on definitions and data sources?

Create a single source of truth through integrated systems and shared dashboards. Start with unit-level metrics that all teams can understand, like cost per customer or revenue per user. Document calculation methods and data sources in a shared workspace that everyone can access and update.

How do we handle qualitative goals like patient outcomes in a KPI framework without gaming the system?

Convert qualitative goals into measurable proxies with clear thresholds. For patient outcomes, track leading indicators like time to diagnosis or treatment completion rates. Use balanced scorecards (frameworks that combine financial and operational metrics) alongside advanced analytics tools to prevent teams from optimizing numbers at the expense of real outcomes.

How often should we review and update our KPI framework?

Review KPI relevance quarterly but avoid changing definitions mid-quarter. Introduce new metrics when you launch major initiatives or enter new markets. Ecommerce companies that maintain consistent measurement frameworks while scaling see better alignment between finance, product, and sales teams over time.

Should we use AI to enhance our KPI tracking from the start?

Start with basic automation before adding predictive analytics layers. Strategic measurement research shows that companies need solid data governance and KPI governance before AI can add value. Focus on automated data collection and simple dashboards first, then explore predictive analytics once your foundation is stable.

Turn Metrics Into Momentum—Without the Overwhelm

The path to implement KPIs without overwhelming the team starts with strategic focus. Choose 3-5 company-level KPIs tied to your growth objectives. Apply the 5/4 guardrail (5 KPIs per team, 4 per role) to prevent metric sprawl. Harvard Business Review research confirms that successful programs align metrics to strategic priorities.

To make this work in practice, lightweight weekly rituals and automated data flows keep tracking simple while driving action. Partnering with a Fractional CFO means your KPI design, data infrastructure, and operating cadence integrate seamlessly from implementation. Building scalable foundations requires this integrated approach.

Start transforming your raw business data into decision-ready dashboards with Ascent CFO Solutions.