How Does a CFO Manage WIP and Cash Cycles in Construction and Real Estate for Sustainable Growth?

Key Takeaways

- Integrating real-time WIP tracking with cash forecasting is essential to prevent cash flow surprises and support sustainable growth in construction and real estate businesses.

- Standardizing processes, automating workflows, and connecting field data to financial reporting enable accurate billing, proactive cash management, and improved decision-making.

- Fractional CFO services provide the expertise and scalable systems needed to transform WIP and cash cycle management into a strategic advantage for growing companies.

A profitable construction project can still bankrupt your company. When work-in-progress reporting lags behind reality and billing cycles misalign with cash needs, even healthy margins become cash flow disasters. The WIP schedules that should provide financial clarity often lag behind field reality, creating dangerous blind spots instead.

This disconnect happens because most companies treat WIP reporting and cash management as separate processes. How does a CFO manage WIP and cash cycles in construction and real estate to prevent this? The answer lies in building a closed-loop system that connects field progress to financial forecasts. When WIP accuracy drives billing discipline, and feeds into 13-week cash forecasts, leaders gain the control and visibility needed to scale confidently.

Ascent CFO Solutions helps construction and real estate companies build these integrated cash flow forecasting systems for sustainable growth.

CFO Playbook: Integrating WIP Management With Cash Cycle Control

Picture this: your project managers report 60% completion, but your billing shows only 45% collected, and your cash forecast assumes draws will hit next week. When these numbers don’t align, you’re flying blind on both profitability and liquidity. To optimize WIP tracking for construction projects, you need a connected process that links project progress, billing cycles, and liquidity planning. The approach centers on one principle: make your financial tracking, billing processes, and cash planning work together as one integrated engine that scales with your growth.

Create Your Single Source of Truth

Start by standardizing cost codes, budgets, and change-order workflows across your ERP, project management, and billing platforms. When field crews use the same cost codes that feed your progress reports and trigger billing actions, you eliminate the manual reconciliation that creates delays and errors. Set up automated workflows so change orders require approval before work begins and immediately update both project budgets and liquidity forecasts. This integration means your construction and real estate financial data flows directly from field to finance without adding overhead as you scale.

Run Monthly Progress Reports That Drive Action

Your monthly progress schedule should tie percent complete directly to field production data and validate estimate-to-complete assumptions with project managers. When progress reports show underbillings, you should trigger immediate billing actions. When they reveal cost overruns, update liquidity forecasts and notify project teams. According to industry guidance, these monthly schedules serve as blueprints for solid construction accounting, helping prevent the cash flow surprises that derail growth plans. Poor progress tracking can also impact bonding capacity and financing, making accurate reporting even more important for scaling companies.

Maintain Your Living 13-Week Liquidity Forecast

Connect your cash planning directly to progress reports and billing schedules so you can time draws, vendor payments, and debt service without surprises. Update this forecast weekly based on project changes, billing milestones, and collection patterns. When your forecast shows potential cash gaps, you have time to accelerate billings, delay non-critical spending, or arrange bridge financing. This approach helps avoid the cash flow blind spots that catch even profitable companies off guard while building repeatable processes that support sustainable growth.

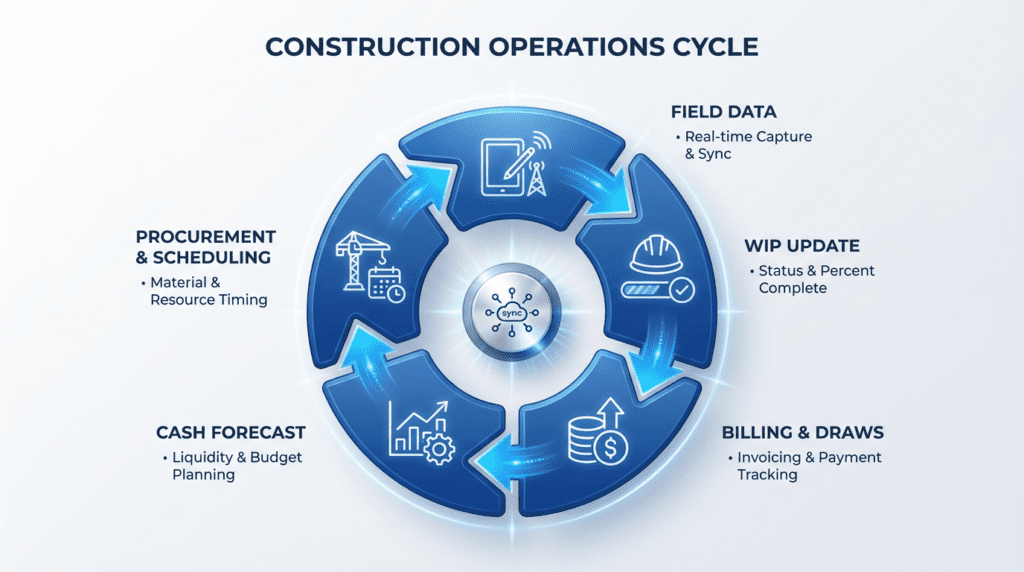

WIP Accuracy: From Field Data To Financial Insight

Building on the integrated CFO playbook, accurate work in progress tracking construction starts with real-time connections between field operations and financial reporting. This creates a feedback loop where project teams spot problems early and finance can trust the numbers driving cash forecasts.

- Connect daily field reports to cost-to-complete calculations by requiring foremen to log quantities completed and project managers to validate percent complete before any WIP entries are posted to the system

- Implement strict change order governance where no additional work begins without approved change orders, and any scope creep automatically triggers margin reforecasting within the same reporting cycle

- Set milestone checkpoints based on your typical project timeline such as early, mid-point, and near-completion reviews that allow teams to validate estimates-to-complete and unlock billing opportunities before cash flow issues develop

- Require cross-functional sign-off on WIP schedules where both operations and finance teams must reconcile percent complete with actual field progress. This happens before monthly WIP schedules are finalized.

- Automate variance alerts that flag when actual costs exceed budgeted amounts by predetermined thresholds, prompting immediate estimate-to-complete reviews rather than waiting for month-end surprises

Professional training organizations like CFMA emphasize that integrating field data with financial reporting creates the foundation for reliable cash flow forecasting. When your construction and real estate team works with experienced fractional accounting support, they can build forecasts that actually predict when cash will hit your account.

Cash Cycle Levers In Real Estate Development

Real estate development presents unique cash flow challenges beyond typical construction projects, requiring coordination of multiple funding sources, extended timelines, and careful balance of pre-sales with construction progress. The best practices for managing cash flow cycles in real estate development center on three strategic levers that protect liquidity while maintaining project momentum.

\

- Structure funding to match milestones: Align draw calendars, interest reserves, and contingency releases to your milestone-based budgets. This prevents front-loaded spending that outpaces financing coverage and ensures you have adequate reserves for each phase of development.

- Optimize working capital timing: Target 40-day DPO where vendor relationships allow, negotiate favorable deposit terms with trades, and stage procurement to match draw timing. Research shows that mid-market companies can significantly improve cash conversion cycles through strategic payables management and liquidity optimization strategies like sweep accounts and ACH payment facilities.

- De-risk through pre-sales and covenant management: Secure customer deposits, letters of credit, and waterfall triggers to reduce exposure. For complex projects, standardize cost codes with 81 core categories to streamline lender reporting and accelerate draw approvals.

These levers work together to create a cash cycle that supports growth rather than constraining it. When integrated with robust cash flow forecasting and experienced Fractional CFO services, developers gain the visibility needed to make confident decisions about new projects and expansion opportunities.

FAQs: WIP And Cash Cycle Management In Construction And Real Estate

Growing construction and real estate companies often struggle with the same operational questions about timing, ownership, and integration. These answers address the most common concerns about how financial leadership impacts project profitability in construction and real estate.

How often should WIP be updated, and who owns the numbers—operations or finance?

Update WIP at least monthly, with weekly updates during active phases. Operations owns field data and percent complete, while finance owns the WIP schedule and margin analysis. Teams must meet monthly to review estimate-to-complete assumptions and validate progress against budgets. The CFMA recommends regular reconciliation between field progress and financial reporting to maintain accuracy.

What KPIs matter most for early warning—under/over billings, ETC variance, DSO, or backlog gross profit at risk?

Focus on three primary indicators: under/over billings ratio, estimate-to-complete variance, and backlog gross profit at risk. These metrics signal cash timing issues and margin erosion before they become problems. DSO matters for working capital, but the first three directly impact project profitability and cash forecasting accuracy.

How do we connect a 13-week cash forecast to lender draws, retainage, and progress billings without manual duplication?

Integrate your project management system with financial reporting to automate data flow. Link milestone completion to draw schedules and retainage release calendars. Use driver-based models that connect percent complete to billing triggers. Fractional CFO services can help establish these integrated systems without requiring full-time overhead.

When should we escalate WIP issues to executive leadership?

Escalate when estimate-to-complete variance exceeds 5% of contract value or when under-billings represent more than 30 days of operating expenses. Flag projects where change orders aren’t approved within your standard cycle. Early intervention protects margins and prevents cash flow disruptions that can impact other projects across your portfolio.

How do we balance accuracy with speed in WIP reporting?

Standardize cost codes and use field productivity benchmarks to validate estimates quickly. Focus detailed analysis on projects over certain thresholds or margin targets. Automate routine calculations while requiring manual review for significant variances. Professional CFO guidance helps build forecasts that drive real decisions while maintaining this balance between precision and practicality.

Scale With Confidence: Turn WIP And Cash Into A Growth Engine

Managing WIP and cash cycles becomes a competitive advantage when you connect field productivity to financial forecasting. The WIP integration transforms project data into actionable cash insights, protecting margins while maintaining liquidity for growth opportunities.

When implemented correctly, your next step: map how WIP updates trigger billing actions and feed into cash forecasting cycles. Construction companies that track key financial metrics consistently outperform peers in both profitability and liquidity planning, enabling sustainable growth.

This performance advantage starts with identifying three fast wins for margin protection and liquidity management. Ascent CFO Solutions provides the fractional CFO services for construction and real estate that turn your WIP reporting into a growth engine.