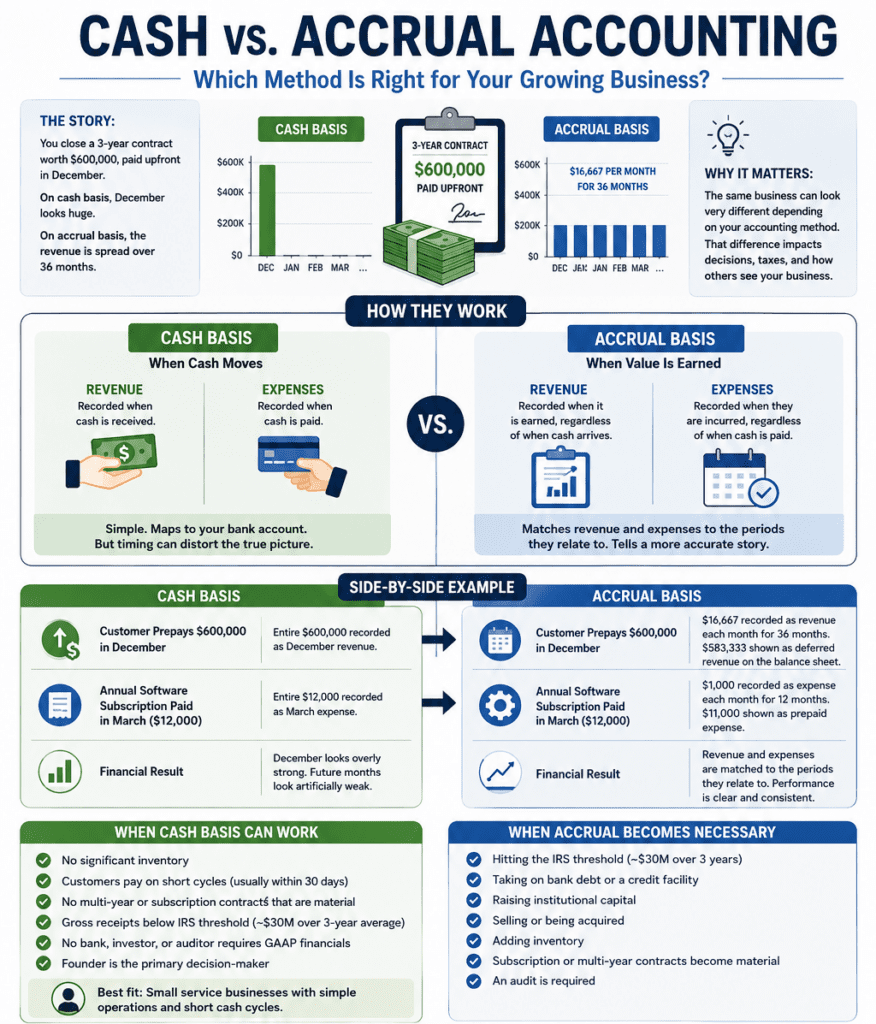

You closed the biggest deal of the year in December. A three-year contract worth $600,000, paid upfront. The check cleared and your team celebrated.

In January, your banker pulls up your financials to review the year. They see a December that looks four times the size of every other month and a January that looks weak. They ask what’s going on. You explain the big December deal. They nod, then ask: “Are you on cash or accrual?”

That’s the moment a lot of founders realize the accounting method they picked years ago has consequences they didn’t anticipate. The same business, with identical revenue and identical customers, can look completely different depending on which method you use. And the difference is not academic. The method you’re on determines how your business looks to investors, lenders, the IRS, and to yourself when you’re trying to make decisions.

This article walks through what each method actually does, why the choice matters more than founders tend to think, and how to know when it’s time to switch.

What Cash Accounting Actually Does

Cash basis accounting records revenue when money comes in and expenses when money goes out. That is the entire method. If a customer pays you in January for work you’ll do across the year, the entire payment shows up as January revenue. If you pay an annual software subscription in March, the entire expense shows up in March.

It’s the simplest way to keep books. It maps cleanly to the bank account. It’s how most very small businesses start. And the IRS allows it for tax purposes for businesses below specific thresholds.

The strength of cash basis is simplicity. The weakness is that it doesn’t reflect the economic reality of the business. A business that just collected a large prepayment looks wildly profitable in the month the cash hits, even though the work to deliver that contract is spread over the next twelve, twenty-four, or thirty-six months. A business that just sent a large invoice but hasn’t been paid yet looks weak, even though it has just earned a large amount of revenue.

For a small consulting firm with short cash cycles and no multi-year contracts, cash basis can work fine. For most businesses past a certain size, it stops telling the truth.

What Accrual Accounting Actually Does

Accrual basis accounting records revenue when it is earned, regardless of when the cash arrives. It records expenses when they are incurred, regardless of when they are paid.

The same $600,000 three-year contract that hits cash basis as a December revenue spike shows up in accrual basis as $16,667 of revenue per month for thirty-six months. The rest sits on the balance sheet as deferred revenue (cash you’ve received but haven’t earned yet). The annual software subscription paid in March gets spread across the twelve months it covers, with the unused portion sitting as a prepaid expense.

This is what GAAP (Generally Accepted Accounting Principles, the standard rulebook for financial reporting in the U.S.) requires. It is what banks, investors, auditors, and acquirers expect to see when they ask for financials.

The strength of accrual basis is that it tells a more honest story about the economic performance of the business. A profitable month looks profitable. A weak month looks weak. Multi-period contracts get smoothed out. Operating performance becomes legible.

The weakness of accrual basis is that it requires more accounting work, more discipline around timing, and a mental model that is less intuitive than “look at the bank account.”

Why the Choice Matters More Than Founders Tend to Think

A founder running on cash basis is not making bad decisions on purpose. They are making decisions on the information their books are showing them. The problem is that cash-basis information can be wrong about the business in three specific ways.

Profitability gets distorted by timing. A founder looking at a cash-basis P&L sees a strong month and assumes the business is strong. The cash-basis P&L doesn’t tell them whether that strength came from operations or from a customer prepayment that doesn’t repeat next month. Decisions made on that picture, like a new hire, a marketing investment, or a piece of equipment, can be made on a misread.

The books don’t survive outside scrutiny. The first time a banker, investor, or acquirer asks for financials, cash-basis books get adjusted to accrual basis by whoever is doing the diligence. The adjustment is often less flattering than the cash version. Founders who go into a lender conversation with cash-basis statements often come out with worse terms, smaller credit lines, or a delay while accrual financials get rebuilt.

The tax position can be wrong. Cash basis has tax advantages in some situations, especially for service businesses with consistent margins. It has tax disadvantages in others, particularly for businesses with significant deferred revenue. A business sitting on $600,000 of cash that represents two years of unearned work pays tax on the full $600,000 in the year it was received under cash basis. The same business on accrual recognizes the revenue, and the tax, over the actual delivery period.

When Cash Basis Still Works

Cash basis is the right method for a narrower set of businesses than most founders realize. The fit profile is:

- The business has no significant inventory.

- Customers pay on short cycles, usually within 30 days.

- There are no multi-year or subscription contracts representing a meaningful share of revenue.

- Gross receipts average below the IRS threshold for required accrual reporting (currently around $30 million over a three-year average, though this changes periodically).

- No bank, investor, or auditor requires GAAP financials.

- The founder is the only stakeholder making major financial decisions.

A small marketing agency billing month-to-month, a freelance consultancy, an early-stage service business under $2M in revenue. These can run on cash basis and produce useful information.

When Accrual Becomes Necessary

The list of triggers that force a move to accrual is longer than most founders expect.

Hitting the IRS threshold. Once a business averages above roughly $30 million in gross receipts over the prior three years, the IRS requires accrual reporting for tax purposes. The threshold adjusts periodically for inflation. Below the threshold, accrual is optional for tax. Above it, it is mandatory.

Taking on bank debt or a credit facility. Most commercial banks require GAAP-compliant accrual financials for loan covenants. A business on cash basis seeking real bank financing usually has to rebuild books in accrual format as part of the loan process.

Raising institutional capital. Any institutional investor, whether venture, growth equity, or private equity, expects accrual financials in diligence. Cash-basis books raise immediate questions about the maturity of the finance function and signal that the company hasn’t yet operated at a level requiring real accounting.

Selling or being acquired. M&A diligence is run on accrual financials. A business that goes into a sale process with cash-basis books will see a meaningful chunk of the diligence period spent reconstructing accrual financials, with the buyer’s team making the calls about how to do it. That work happens under the buyer’s lens, not yours.

Adding inventory. Businesses that hold inventory have to use accrual for tax purposes above small thresholds. Inventory accounting requires using the accrual method to function correctly.

Subscription or multi-year contracts becoming material. Once recurring or multi-period revenue is more than a small share of the business, cash basis distorts the picture so significantly that even internal decision-making becomes unreliable.

An audit. Any audited financial statement is, by definition, accrual. Cash-basis statements cannot be audited under GAAP.

Talk to a CFO

If you are running on cash the basis and any of the triggers above are within twelve months of your business, the conversation about converting is one to have now rather than later. A clean conversion done a year in advance is a routine project. A conversion done during a fundraise, a sale, or a loan process is a fire drill.

Get right-sized financial leadership from experienced CFOs ready to lead your team.

The Mistakes Founders Make When Switching

Most cash-to-accrual conversions are not technically difficult. The mistakes founders make are timing and process mistakes, not accounting mistakes.

Switching during a crunch. The right time to switch is when nothing important is happening. The wrong time is during a fundraise, a sale process, or a loan close. A conversion done under pressure is rushed, error-prone, and produces accrual financials that do not fully match the underlying business reality. A conversion done in a quiet quarter is clean.

Switching without a proper opening balance sheet. The conversion requires building an opening accrual balance sheet at the cutover date, with accounts receivable, accounts payable, deferred revenue, prepaid expenses, and accrued expenses all captured correctly. Skipping this step produces books that look right month-over-month but do not tie to the underlying economic reality of the business at the cutover point.

Not retraining the team and leadership. Accrual basis introduces concepts that don’t exist in cash accounting: deferred revenue, accrued expenses, prepaid balances, the difference between cash and earnings. The team has to learn to read the new P&L and balance sheet, and the team has to learn to maintain them. That training is part of the conversion, not an afterthought.

When to Make the Switch

For most growth-stage businesses, the right time to switch is at least twelve months before any of the major triggers. That means twelve months before a planned raise, twelve months before a sale process, twelve months before a loan application, or twelve months before hitting the IRS threshold.

Many companies will want to consider retroactively restating at least one year of the books to accrual accounting so that you can have a year-over-year comparison.

That window allows the new books to settle, to produce a clean year of accrual financials, and to give whoever is reviewing those financials, whether an investor, a buyer, a banker, or an auditor, a full year of comparable data. Books with three months of accrual history and nine months of “we just converted” are weaker than books with twelve months of clean accrual reporting.

If the triggers are already within six months, the switch should happen immediately. The shorter the window, the more urgent the work.

FAQs About Cash vs. Accrual Accounting

1. Can a business use different methods for tax purposes and financial reporting?

Yes, with limits. A business can run its internal financial reporting on accrual basis, for management visibility, investor reporting, and bank relationships, while still filing taxes on cash basis if it qualifies for cash basis under IRS rules. This is common for businesses that are growing toward the threshold but haven’t crossed it yet.

2. How long does a cash-to-accrual conversion take?

A typical conversion for a $5M to $20M business takes between two to six weeks, including the opening balance sheet construction, any parallel reporting period, and team training. Larger or more complex businesses may take longer.

3. Does cash basis save on taxes?

Sometimes, but not always. Cash basis tends to favor businesses that consistently have more accounts receivable than accounts payable, where revenue earned has not yet been collected and exceeds expenses incurred but not yet paid. It can hurt businesses with significant deferred revenue or long collection cycles. The actual tax impact depends on the specific balance sheet profile and should be modeled before assuming a benefit.

4. What’s the difference between accrual basis and GAAP?

Accrual basis is the foundational method GAAP uses, but GAAP includes many additional rules beyond just accrual timing: revenue recognition standards (ASC 606), inventory accounting, lease accounting, stock-based compensation, and many others. A business can be on accrual basis without being fully GAAP-compliant. Most businesses preparing for outside capital or a sale need both: accrual basis and GAAP-compliant treatment of the major accounting areas.

5. What if I’m already on accrual but my books are messy?

The conversation is different. The issue is not method, it is quality. Most diligence and lender pushback comes from accrual books that aren’t being maintained correctly: deferred revenue that isn’t being released on schedule, prepaid expenses that aren’t being recognized, balance sheet accounts that don’t tie out. The fix is a cleanup project, usually scoped against a target deadline like a raise, a sale, or a loan close.

The Right Time to Have the Conversation Is Before You Need the Right Answer

The founders who run into the cash-vs-accrual question at the worst time are usually the ones who didn’t realize it would matter until it did. The lender asked. The investor asked. The buyer asked. The auditor asked. By then, the answer “we’re on cash basis and we’ll convert as soon as we can” is already costing them leverage in whatever conversation they’re trying to have.

We help founders and CEOs of growth-stage companies nationwide build financial infrastructure that holds up to outside scrutiny. Through our fractional CFO services, we run cash-to-accrual conversions, set up GAAP-compliant reporting, and put the financial discipline in place before the moment that demands it.Book a CFO strategy call with Ascent CFO Solutions and get the right accounting method in place for the next stage of your business.

Contact Us

Questions or business inquiries regarding our part-time CFO, finance and accounting services are welcome at: info@ascentcfo.com