Key Takeaways

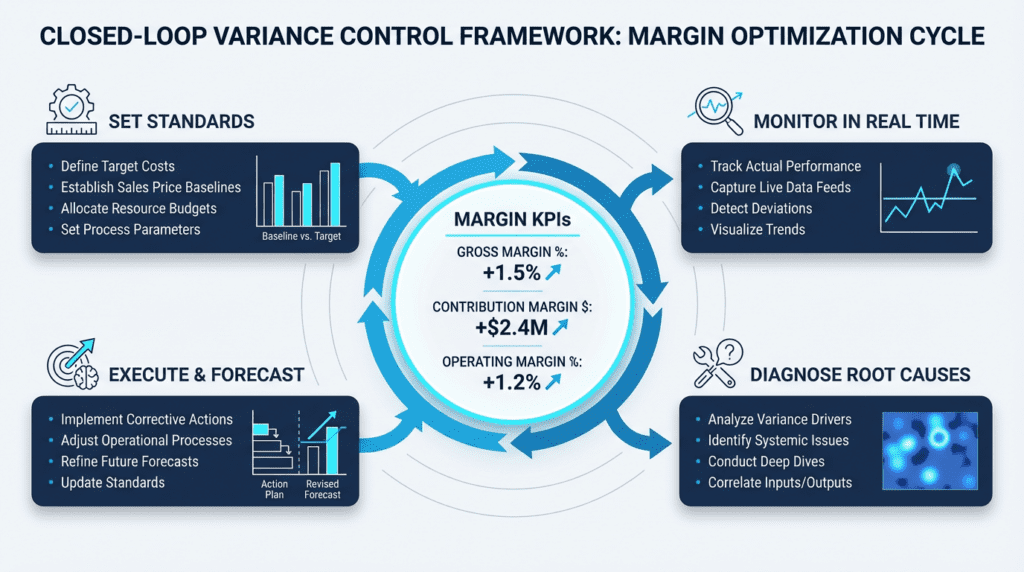

- A closed-loop system—combining standard setting, real-time monitoring, root-cause analysis, and accountability—enables CFOs to proactively manage manufacturing cost variance and protect profit margins.

- Integrating data from ERP, MES, and purchasing systems into unified business intelligence dashboards provides live visibility, allowing for rapid detection and resolution of cost variances.

- Prioritizing high-impact drivers like material costs and implementing disciplined variance review routines can yield significant margin improvements within a single quarter, especially with expert guidance from fractional CFO services.

Manufacturing cost variance can silently drain 3-8% from your profit margins before you even notice. While your production team focuses on output and quality, small deviations in material costs, labor efficiency, and overhead absorption compound into significant profit leaks. The question isn’t whether variance exists, but how can a CFO reduce manufacturing cost variance before it undermines your growth trajectory. The good news is this challenge has a systematic solution.

Experienced Fractional CFOs use a closed-loop system that connects standard setting, real-time monitoring, root-cause analysis, and accountability to your margin targets. This approach transforms variance from an inevitable cost of doing business into a manageable driver of margin improvement. We’ll explore the specific strategies, data analytics tools, and leadership routines that manufacturing companies use to turn variance control into sustained profitability.

Ready to stop profit leaks and build systematic margin protection? Ascent CFO Solutions provides the experienced financial leadership to design and implement variance control systems that scale with your growth.

Strategies a CFO Can Use to Minimize Manufacturing Cost Variance

When your manufacturing costs swing unpredictably month to month, it becomes nearly impossible to forecast margins accurately or make confident pricing decisions. What strategies can a CFO use to minimize manufacturing cost variance while maintaining operational flexibility? The answer lies in building a closed-loop control system that prevents variance before it happens and catches deviations quickly when they do occur. This approach transforms cost management from reactive problem-solving into proactive margin protection.

Lock Down Your Standards With Engineering Approval Controls

Manufacturing variance often starts with loose standards that drift over time. Bills of materials and process modifications happen without proper oversight, creating costs that creep up each month. Require approval from both engineering and finance teams before any recipe or process adjustments take effect. Modern systems offer engineering change management features that track every revision with approval workflows and automatic release controls. This prevents unauthorized modifications that silently erode your margins.

Build Live Visibility Into Your Operations

You cannot manage what you cannot measure immediately. Integrate your ERP, manufacturing execution systems, and purchasing data into business intelligence dashboards that track purchase price variance, material usage, labor efficiency, and overhead absorption continuously. This creates one reliable data source and eliminates delays in spotting problems. Manufacturing companies face unique challenges with complex cost structures, making integrated reporting systems essential for maintaining control.

Establish Weekly Variance Reviews With Clear Accountability

Turn monthly variance surprises into weekly problem-solving sessions. Assign specific owners to each variance category and apply root-cause analysis techniques like the 5-Why method to identify true drivers. Connect these corrective actions to your 13-week rolling forecast so improvements show up in projected margins, not just meeting minutes. Fractional CFO services can help you design and implement these integrated systems without the cost of hiring full-time technical staff.

Tools That Help CFOs Analyze and Control Cost Fluctuations

The right technology stack transforms manufacturing cost fluctuations from monthly surprises into predictable, manageable processes. Effective cost control requires integrated systems that capture both planned standards and actual performance in real time.

- Unify your data sources by connecting ERP standards with MES (Manufacturing Execution System) actuals and purchasing data through business intelligence dashboards

- Build variance waterfalls that break down total cost differences into price, mix, yield, labor, and overhead components for targeted action

- Deploy control charts using statistical process control methods to separate normal fluctuation from meaningful trends

- Create SKU-level margin trees that connect product profitability to specific cost drivers and production lines

- Apply ABC analysis to focus improvement efforts on the 20% of products that drive 80% of your variance impact

These tools work best when implemented as an integrated system rather than standalone solutions. Fractional CFO expertise can help design the right combination for your manufacturing environment and growth stage.

How Financial Leadership Reduces Variance Day to Day

Financial leadership drives accountability by aligning plant incentives with variance outcomes and establishing clear ownership structures. Tie plant bonuses to both variance reduction and on-time delivery to prevent teams from gaming one metric at the expense of another. Publish a simple RACI matrix so every adverse variance has an assigned owner within 24 hours, creating the urgency needed for rapid root-cause analysis. This approach transforms variance from a monthly reporting exercise into a daily operational priority that manufacturing CFOs can monitor and influence in real time, often supported by virtual CFO services that provide the expertise to implement these systems effectively.

Effective CFOs focus their energy where materials typically represent 60-70% of total costs rather than focusing on low-impact overhead adjustments. Prioritize purchase price variance (PPV), supplier contract terms, and yield improvements over minor labor efficiency tweaks that barely move the profit needle. According to FP&A best practices, successful cost management requires strategic focus on high-impact drivers. Start with a disciplined pilot on your top-volume SKUs, lock the lessons learned into standard operating procedures, then scale plant-wide to prevent backsliding into old habits.

FAQ: Reducing Manufacturing Cost Variance

Manufacturing leaders often struggle with setting realistic expectations for variance reduction and knowing where to focus first. The following guidance provides practical benchmarks and timelines based on real-world CFO experience.

What are realistic variance targets for materials, labor, and overhead?

Material variances should stay within 2-5% of standard cost for stable products, with tighter control for high-volume items. Labor efficiency typically ranges 5-10% depending on product complexity. Overhead variances need budgets that adjust when production volume changes. Set tolerance bands using 13-week rolling averages rather than monthly snapshots to smooth seasonal swings.

Which variances should get priority attention from leadership?

Focus where dollars are largest, not percentages. If materials represent 70% of your cost structure, a 2% material variance outweighs a 10% labor variance. Use variance analysis to rank by absolute dollar impact. Address recurring problems before one-time events. Manufacturing companies typically see the biggest returns from supplier management and waste reduction programs.

How should a CFO separate volatile input prices from shop floor usage issues?

Track purchase price variance separately from material usage variance in your ERP system’s standard costing reports. Price volatility comes from market forces outside your control. Usage problems show up in waste, scrap, and cycle time data that your teams can directly influence. Focus operations on controllable factors while using supplier contracts to manage price risk.

What improvements can a plant expect in 13 weeks without disrupting output?

Most plants can reduce material waste by 15-20% and improve labor efficiency by 10-15% within one quarter by focusing on high-volume products first. Start with your top 20% of SKUs by volume. Avoid changing multiple standards simultaneously. Virtual CFO services can help design the rollout sequence to maintain production stability while capturing measurable wins.

How often should variance targets be updated?

Review standards quarterly but avoid constant changes that confuse operations teams. Update material costs when supplier contracts renew or product designs change significantly. Labor standards need adjustment when processes improve or equipment upgrades occur. Balance accuracy with stability by using clear effective dates and avoiding mid-month changes that disrupt reporting cycles.

Next Steps: Turn Variance Into Margin With a Fractional CFO

Manufacturing cost variance need not erode your profit margins. The closed-loop system requires disciplined leadership to set standards, monitor real-time data, and drive accountability. Fractional CFO services provide this expertise without the full-time executive cost.

The path forward is straightforward. Gather your last two months of BOM versions, PPV reports, and scrap data. A structured diagnostic can transform this information into a 90-day roadmap with a 3-metric scorecard tied directly to profit improvement.

Schedule a no-obligation variance diagnostic with Ascent CFO Solutions to design your closed-loop system and embed the weekly cadence that turns cost control into competitive advantage.

Contact Us

Questions or business inquiries regarding our part-time CFO, finance and accounting services are welcome at: info@ascentcfo.com